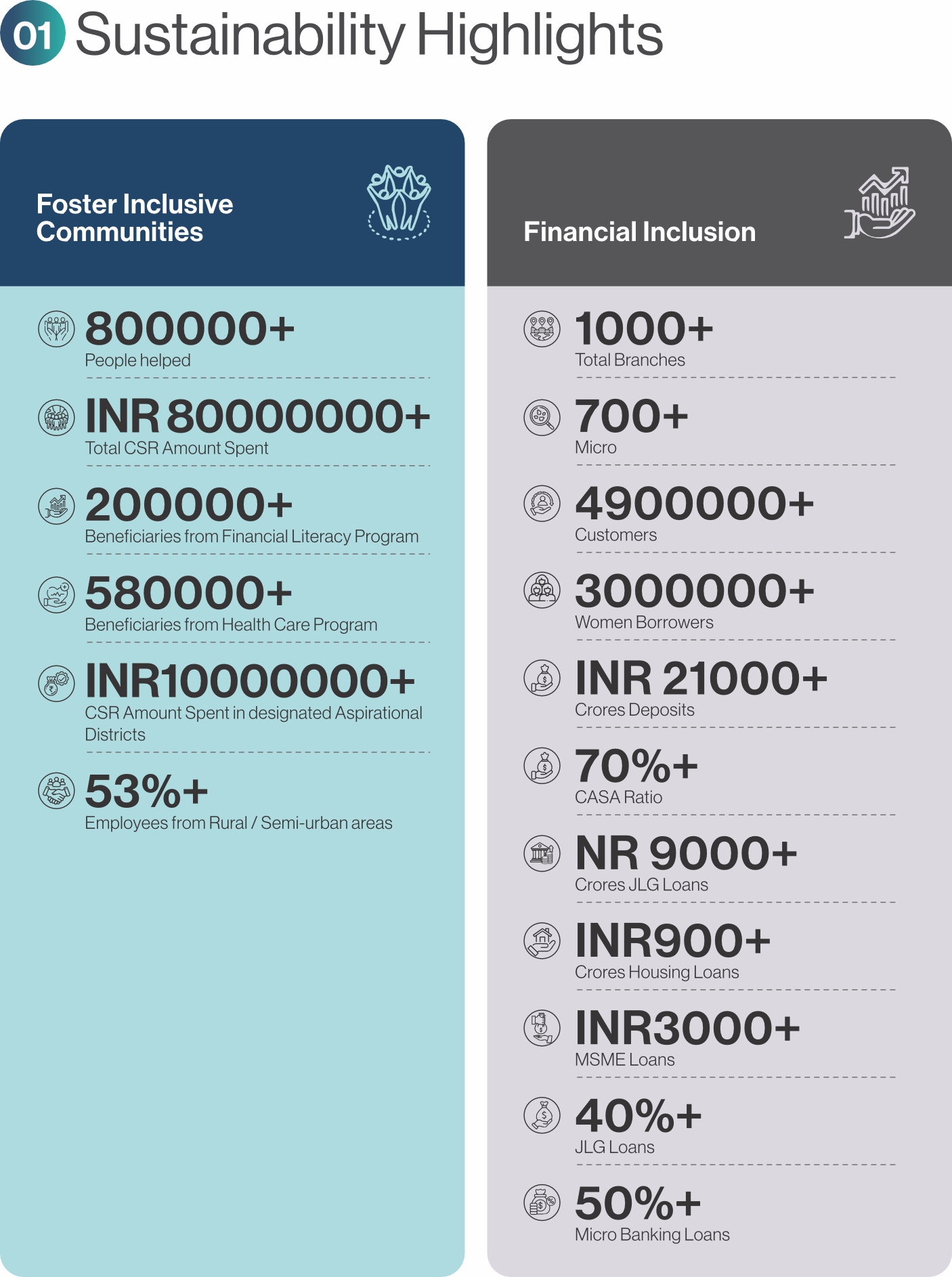

Sustainability Highlights

About the Report

Utkarsh Small Finance Bank Limited is happy to present its 2nd Annual Sustainability Report providing transparency and accountability regarding our sustainability performance for a reporting period of April 01, 2024 to March 31, 2025. We are committed to increasing

Reporting Frameworks and Benchmarks

The data and topics that are included in this Report are guided and informed by the GRI reporting standard. The GRI standard is one of many recognized ESG reporting frameworks that provide topics, structure and advise companies on which ESG data and information to disclose. This makes company disclosure comparable across the industry. The GRI framework is one of the most widely used reporting frameworks and contains universal, topic and sector standards, which are used together to comprehensively disclose and organize ESG reporting. GRI reporting topics are voluntary, but GRI itself is a tool that demonstrates our commitment to reporting transparency

In addition, we have used SASB Standards, BRSR Reporting, PRB (Principles of Responsible Banking) along with linkages to the United Nations Sustainable Development Goals (UN SDGs).

transparency and voluntary disclosure about our business and operational activities. This report reflects our impact across key topics and issues that are important to both our business and our varied and diverse stakeholders. This report aims to offer our stakeholders

Scope and Reporting Boundary

The reporting boundary encompasses all of Utkarsh Small Finance Bank’s operations, including our headquarters in Varanasi, Regional Offices and Branch offices spread across the country.

Responsibility Statement

This report is a fair representation of Utkarsh Small Finance Banks’ financial, non-financial, sustainability, and operational performance for FY2024-25 and

a comprehensive assessment of Utkarsh Small Finance Bank’s Sustainability vision, performance, and initiatives, all of which materially influence our business

Communication of Feedback

Utkarsh Small Finance Bank actively encourages feedback from stakeholders to continuously improve our sustainability efforts. Stakeholders can provide their input and comments through various channels, including the company’s website, dedicated email address (secretarial.usfb@utkarsh.bank), and during stakeholder engagement sessions. Additional information about Utkarsh Small Finance Bank’s sustainability initiatives and access to this and future sustainability reports can be found on the company’s official website: C:\Users\shumailatambe\Documents\Utkarsh\www.www.utkarsh.bank https://www.utkarsh.bank/

About the Company

Geographical Reach

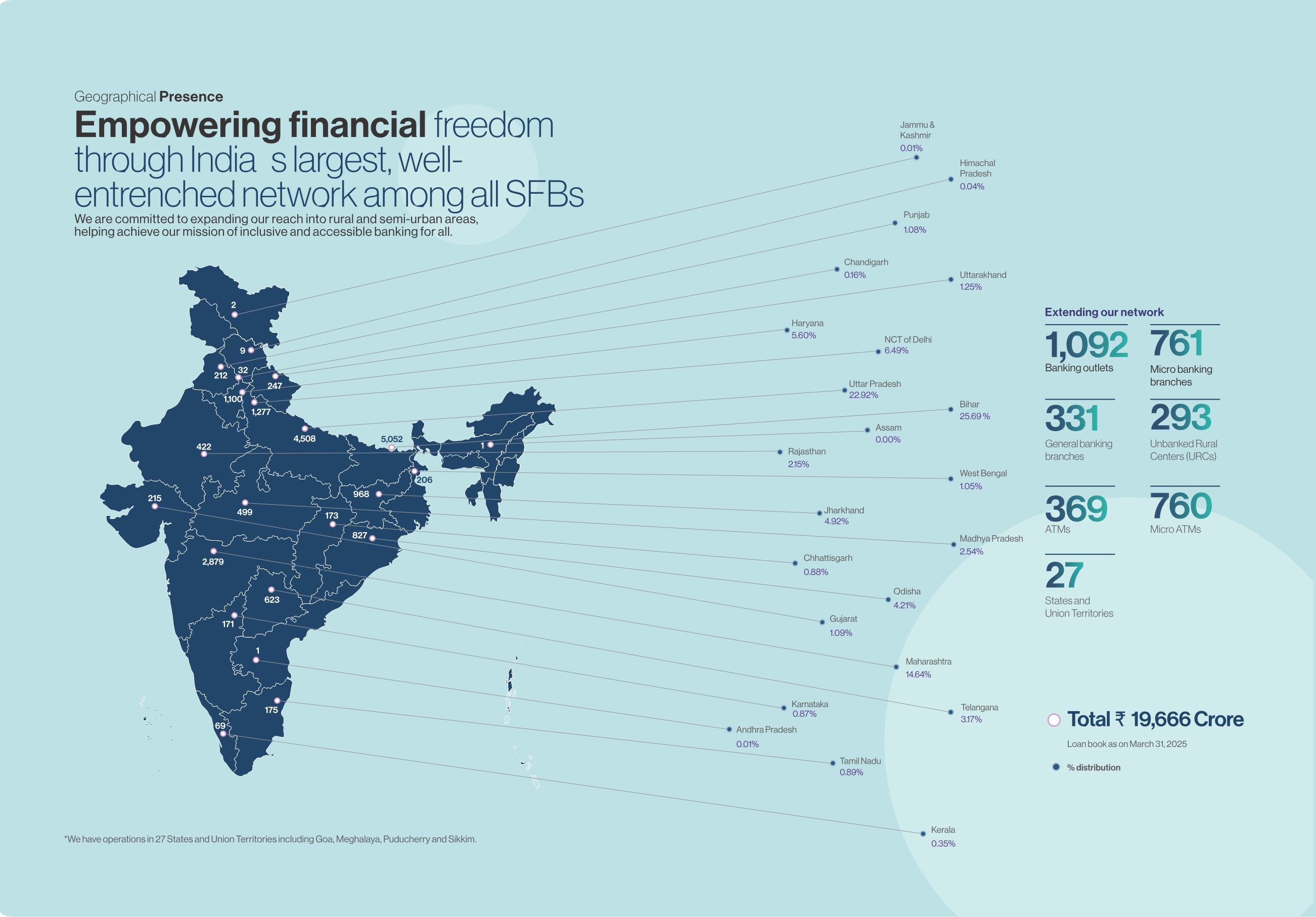

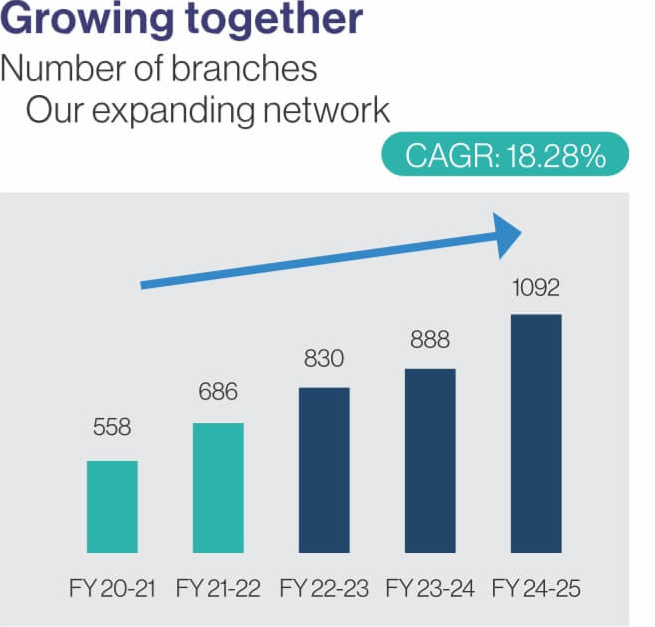

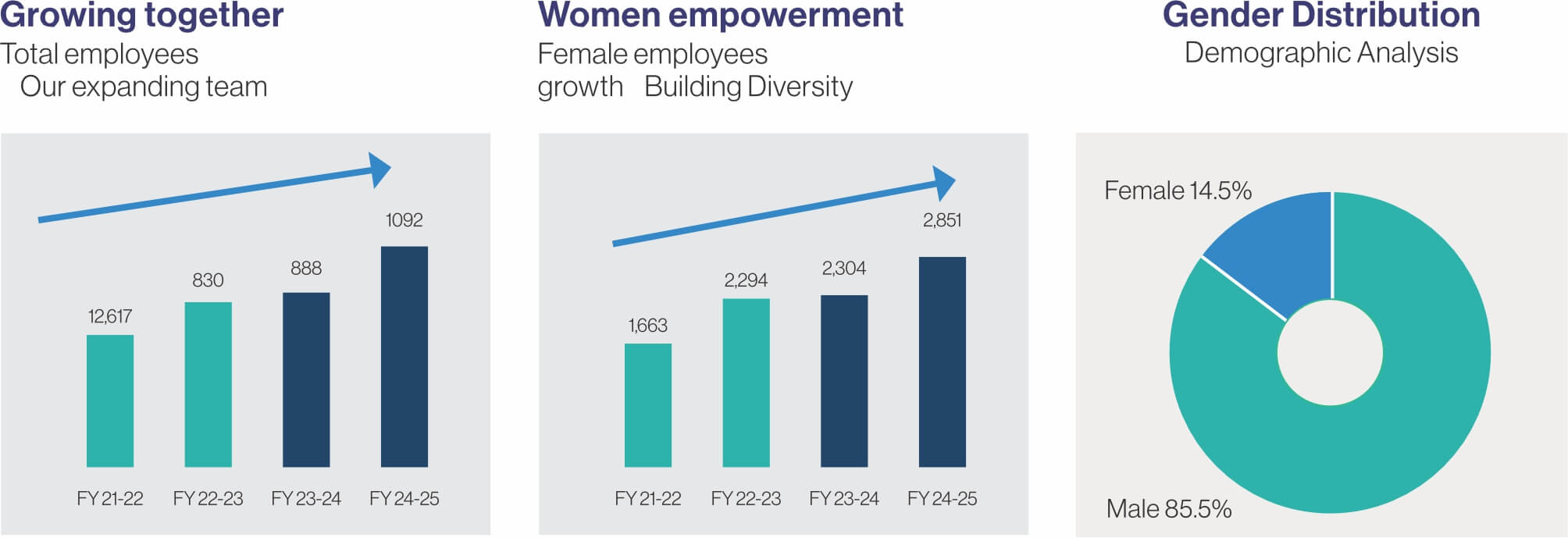

Utkarsh Small Finance Bank has established a significant geographical footprint, operating 1,092 banking outlets across 27 states and union territories as of March 2025. We have built our strongest networks in Bihar and Uttar Pradesh, which together contribute to nearly half of both our branch presence and gross loan portfolio, demonstrating our commitment to serving regions with a high need for inclusive financial solutions. Over recent years, we have strategically expanded our operations beyond our heartland, reaching communities in metro, semi-urban, and rural locales for broader financial inclusion.

- Message from Chairman

- Message from CEO

- Advancing our Sustainability Strategy

Message From Chairman

I am privileged to present the Sustainability Report for FY 2024-25, marking another milestone in Utkarsh Small Finance Bank’s journey towards responsible and inclusive growth. As Chairman, I view sustainability not merely as a compliance obligation

but as a long-term strategic imperative that shapes our institutional legacy and aligns with the Principles of Responsible Banking.

Dear Stakeholders,

Over the past year, we have successfully expanded our footprint to 1,092 branches across 27 states and Union Territories,

reflecting our determination to reach underserved populations. This expansion is guided by our commitment to align business growth with

India’s net-zero goals, the Paris Agreement, and the UN Sustainable Development Goals, ensuring that we contribute to both national and

global priorities.

Our green infrastructure, anchored by the GRIHA 5-star certified Utkarsh Tower, demonstrates how business operations

can minimize environmental impact while promoting resilience. Reductions of 40% in energy consumption and 70% in water usage, along with solar

energy meeting nearly 15% of our needs, demonstrates how setting measurable targets enables us to create positive outcomes and reduce negative

impacts.

Social inclusion remains at the heart of our business. With over 30 lakh women customers, women-led branches, and a substantial

number of women employees, we are not only providing access to finance but also empowering individuals and communities to build long-term

independence and security. By offering bespoke products to underserved groups, we act as responsible partners to our clients and customers,

supporting practices that enhance sustainable livelihoods.

Sincerely,

Parveen Kumar Gupta

Chairman

Utkarsh small Finance Bank Limited

Message from MD & CEO

It is my honour to share the FY 2024-25 Sustainability Report, showcasing the tangible strides Utkarsh Small Finance Bank has made towards embedding sustainability into our business operations, customer engagement, and community impact.

Dear Customers, Partners, and Colleagues,

Our digital transformation efforts gained strong momentum this year with more than 21 lakh accounts opened through innovative

digital platforms such as V-KYC and UPI Lite. This progress enabled a significant move towards paperless banking, reducing our environmental

footprint by saving millions of sheets of paper annually. At the same time, it enhanced financial accessibility for rural and underserved

populations, reinforcing our mission of inclusive banking.

In FY 2025, we also achieved an important milestone by undertaking greenhouse

gas emission calculations for the first time. By measuring Scope 1 and Scope 2 emissions across our head office, branch network, and ATMs,

we have established a clear baseline that will guide our future carbon reduction and energy efficiency initiatives. This step marks the beginning

of a more structured journey towards climate responsibility.

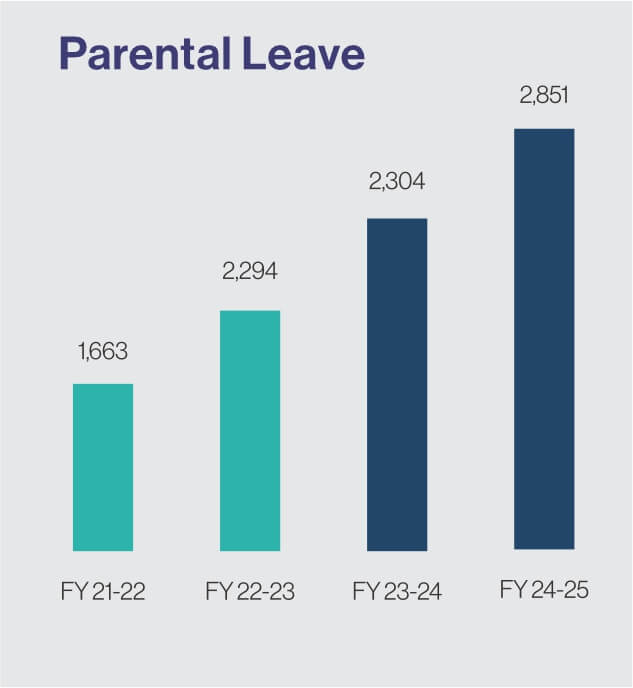

Our workforce diversity continues to be a source of strength, with over 2,300 women

employees and multiple women-led branches representing our belief that inclusive growth starts from within. This commitment is also visible in our

tailored financial products that have positively impacted the lives of over 30 lakh women customers, enabling greater autonomy and socio-economic

empowerment in communities previously marginalized

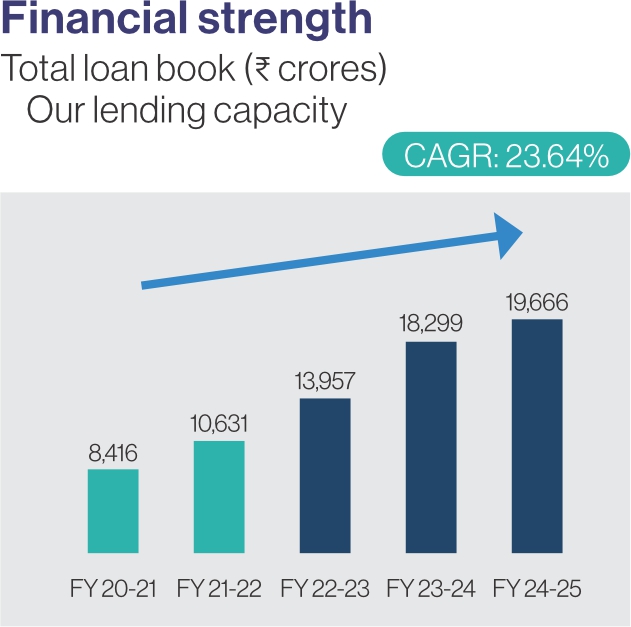

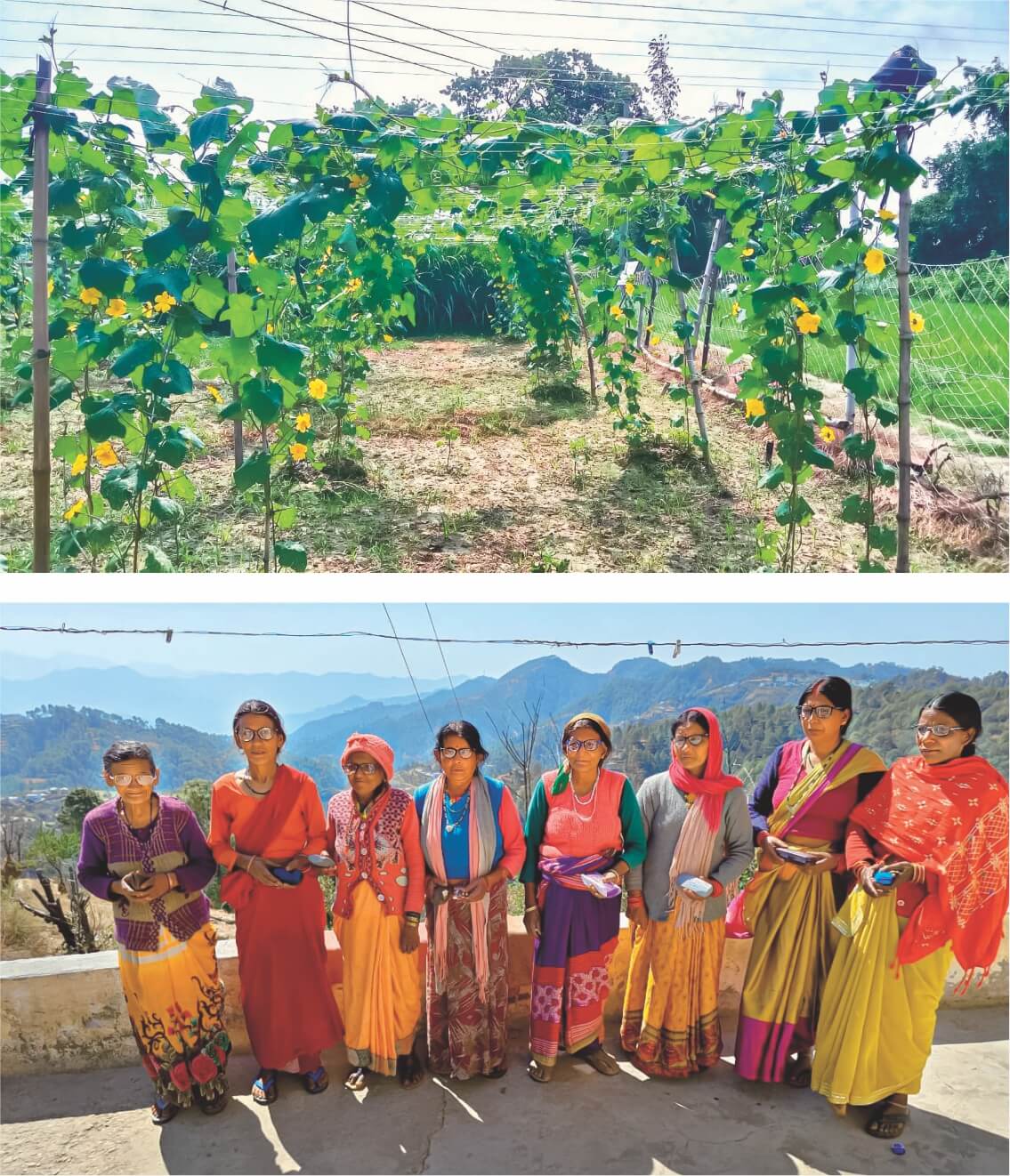

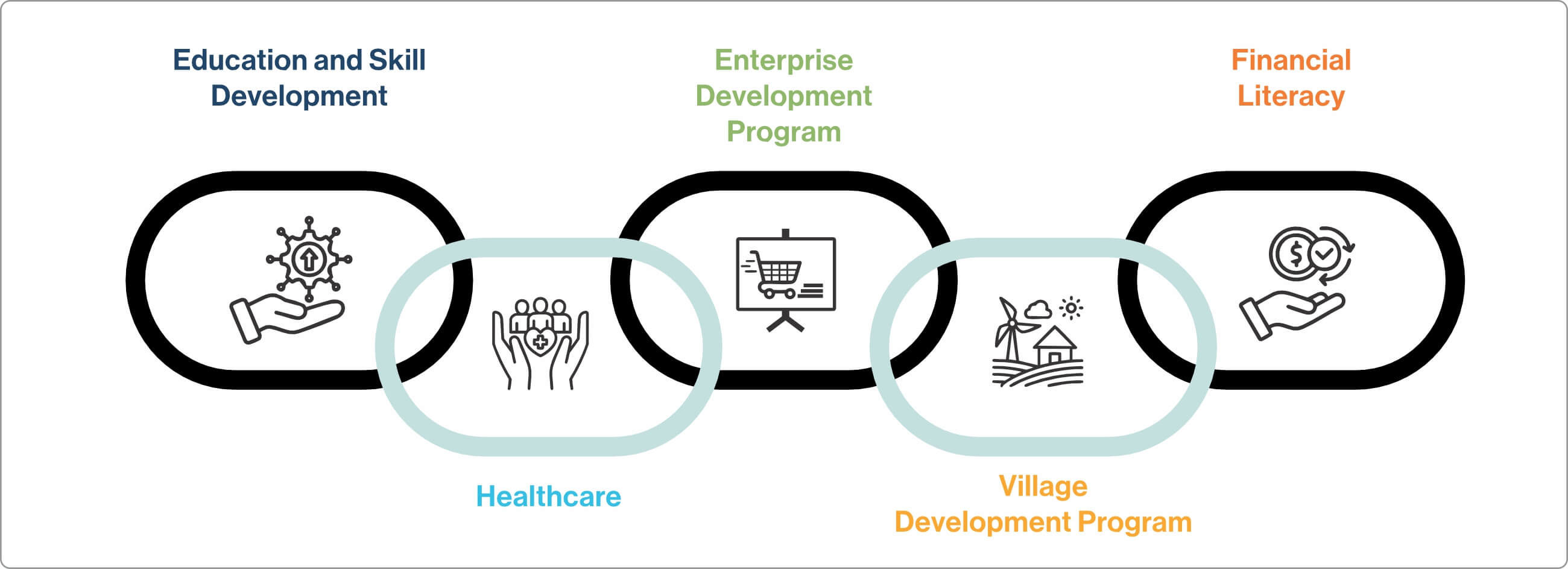

Operationally, the Bank demonstrated resilience and prudence during the year. Deposits grew by 23.4 percent to H21,566 crore, while the gross loan portfolio expanded to H19,666 crore. Despite wider economic challenges, we maintained robustasset quality and strong capital adequacy and liquidity ratios, underscoring our disciplined approach to risk management.Governance has been further strengthened with enhancements to our cybersecurity and data privacy frameworks, alongside the integration of climate-related financial risk assessments into our lending and investment decisions. Regular materiality assessments ensure that our ESG priorities remain relevant and aligned with regulatory requirements and global frameworks such as the GRI. A vital part of our internal sustainability journey has been the focus on employee capability building. This year, we expanded training programs that cover risk management, digital banking, financial inclusion, customer service excellence, and leadership development. These initiatives are cultivating a culture of continuous learning and equipping our teams to meet the evolving needs of customers responsibly.Our corporate social responsibility programs, implemented through the Utkarsh Welfare Foundation, impacted more than 11 lakh lives during the year. Flagship initiatives such as the Mahila Udyami Sashaktikaran Programme supported women entrepreneurs with capacitybuilding and financial independence, while the Village Development Programme promoted sustainable livelihoods through activities such as mushroom cultivation, backyard poultry, and agricultural training. Smart Classes and Nutrition Gardens improved learning environments and child health in government schools, and E-Clinics launched in Uttar Pradesh and Bihar, alongside healthcare support in Meghalaya, expanded access to primary healthcare services. In addition, polyclinic health camps, sanitary napkin vending initiatives, and livelihood programs for artisans and weavers strengthened community well-being and resilience. In the state of Uttarakhand, Utkarsh Welfare Foundation hasbeen actively working in the districts of Almora, Dehradun,Haridwar, and Udham Singh Nagar. With a vision to promotesustainable development and enhance community wellbeing, these initiatives empower rural households through livelihood enhancement, healthcare, financial literacy,education, and women’s empowerment. In FY 2024–25, theFoundation positively impacted nearly 2.6 lakh lives in the region. Livelihood programs focused on organic farming,backyard poultry, and mushroom cultivation are helpingfamilies strengthen economicsustainability. Smart Classes in government inter colleges andcomputer literacy training underthe Education Programme areenhancing digital and academic learning. On the health front,E-Clinic services, the SwasthyaMitra initiative, and healthawareness programs are bringingaffordable, quality healthcarecloser to rural communities. Inaddition, the Financial AwarenessProgramme is connecting familiesto government schemes, buildingfinancial literacy, and enablingprudent economic decisions,fostering resilience and long-termsecurity. Looking ahead, sustainability remains central to the Bank’s vision, driving innovation, responsible growth, and social empowerment. I extend my heartfelt gratitude to our employees, customers, board members, investors, and partners for their trust and continued collaboration. Together, we will build a future where financial progress goes hand in hand with environmental stewardship and inclusive development

Warm Regards,

Govind Singh

Managing Director & CEO

Utkarsh Small Finance Bank Limited

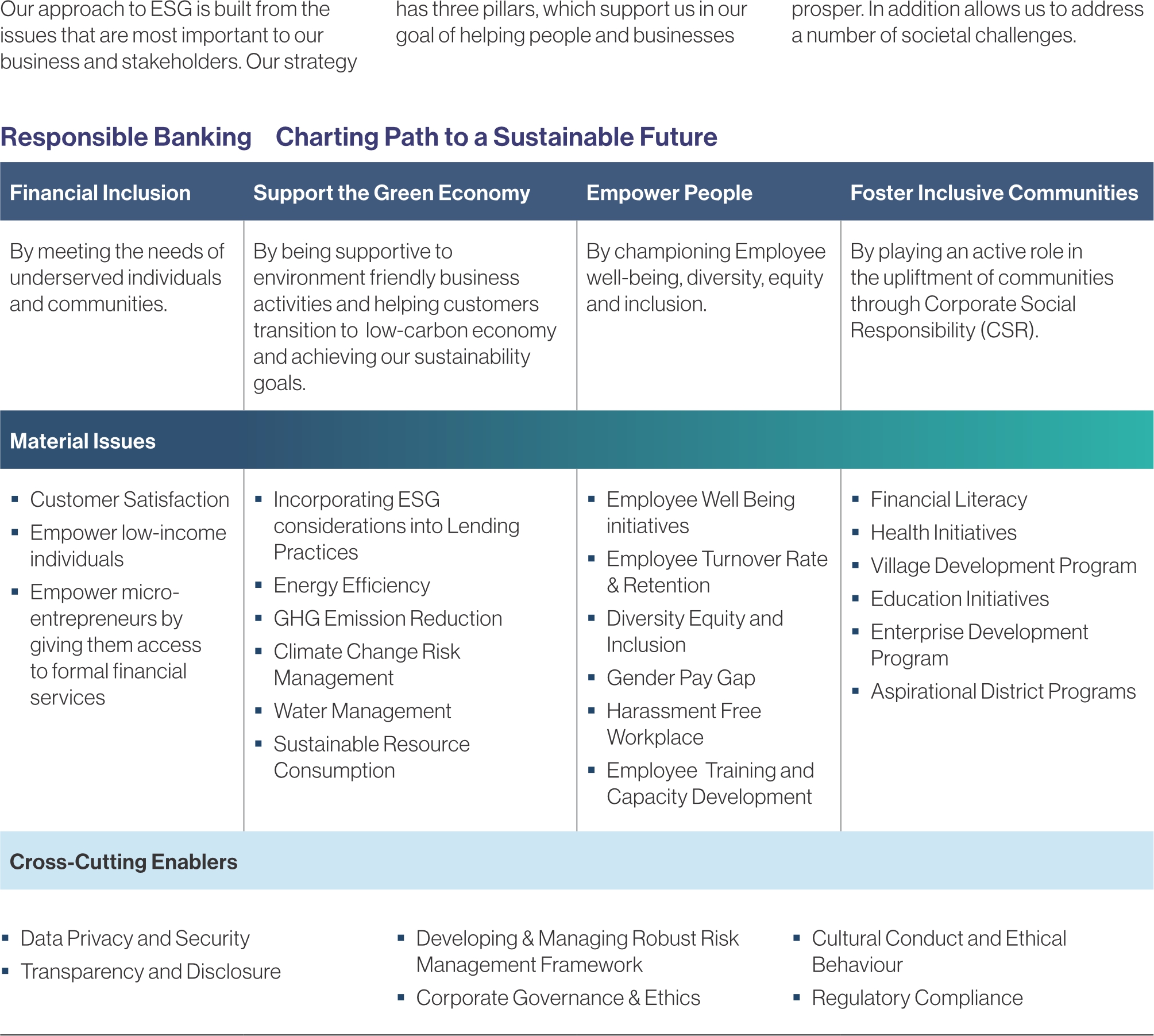

Advancing our Sustainability Strategy

Our approach to ESG is built from the issues that are most important to ourbusiness and stakeholders. Our strategy

has three pillars, which support us in our goal of helping people and businesses

prosper. In addition allows us to address a number of societal challenges.

- Stakeholder Identification & Channels of Communication

- Material Issues from Stakeholder Engagement

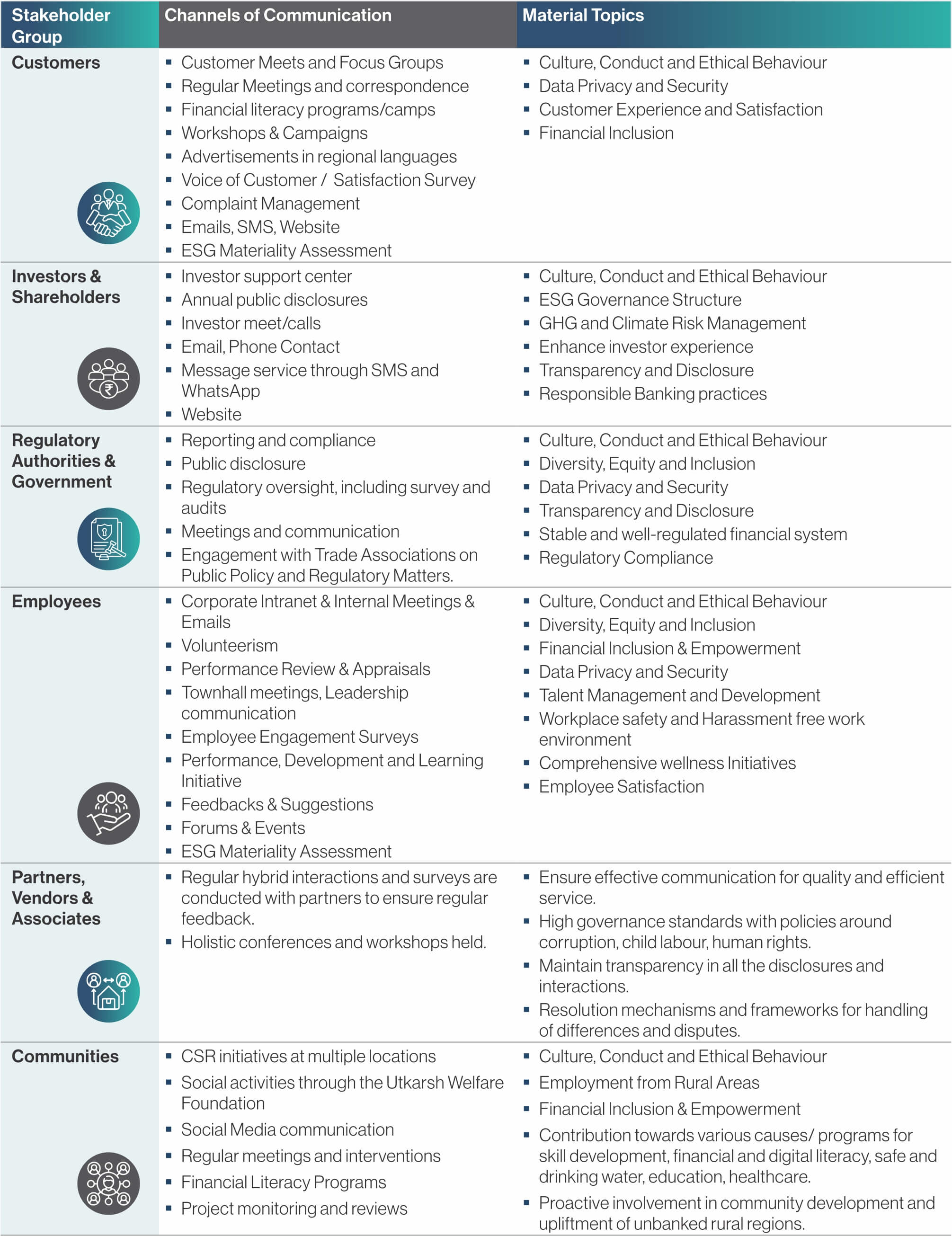

Stakeholder Identification & Channels of Communication

Utkarsh Small Finance Bank’s stakeholders fall within the following broad categories: Customers, Employees, Communities, Investors, Government and Value Chain Partners.

The Bank prioritizes transparent and open communication and engagement with its stakeholders. The valuable feedback from these stakeholders is crucial in enhancing the Bank’s business

strategies and risk management practices. This feedback enables the

Bank to refine its internal processes, capitalize on business opportunities, reduce operational uncertainties, and maintain a competitive edge, all while delivering value to every

stakeholder involved. Communication channels and material topics are further defined below

Material Issues from Stakeholder Engagement

- Methodology and Process

- Materiality Matrix

- ESG Risks & Opportunities

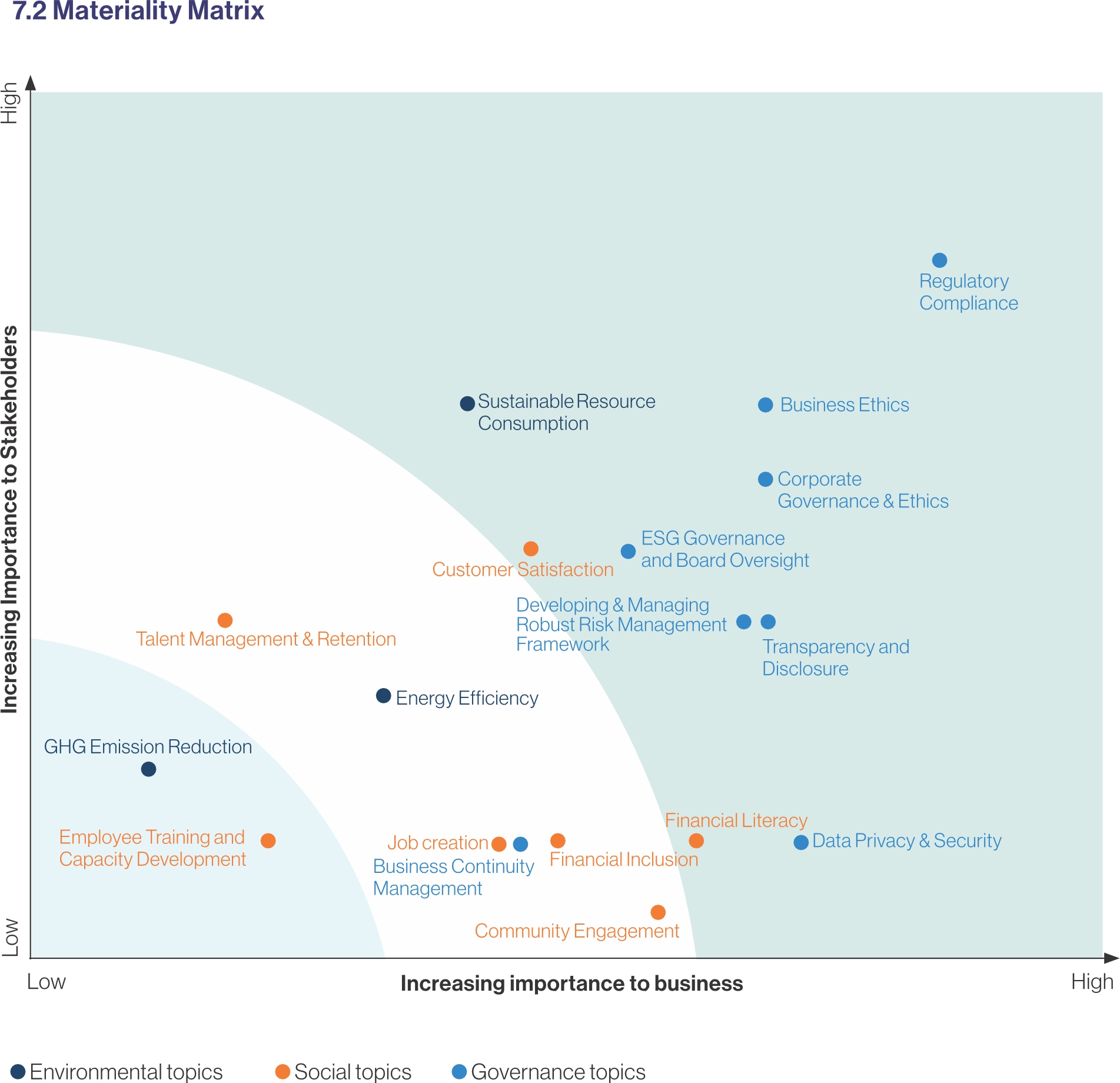

Methodology and Process

To effectively focus our ESG strategy, our company stakeholders both internal and external, participated in an issue prioritization exercise to identify our most material ESG issues

in terms of importance to our business and our community. This exercise identifies a range of issues across the ESG categories. Ultimately issues are prioritized and plotted on a matrix, which ranks

issues based on impact to our business and our community.The Bank conducted this assessment through interviews, surveys and

research with key stakeholders. Stakeholders included, but were not limited to, our executive and board leadership, investors, customers, colleagues, non-profit and community partners,

regulators and peers.Our assessment methodology aligns to Utkarsh Small Finance Bank’s broader methodology and included three phases: 1. Material topic identification: Develop a preliminary list

of topics based on a variety of internal and external sources

2. Stakeholder input collection:Conduct surveys, interviews and research to capture stakeholder input 3. Scoring and validation: Assign weights to different topics

and generate materiality matrix. The issues identified in this prioritization will drive our ESG strategy and reporting in the years ahead. The X-axis of the materiality assessment graph implies importance

to business whereas the Y-axis implies importance to the Bank’s stakeholders.

Materiality Matrix

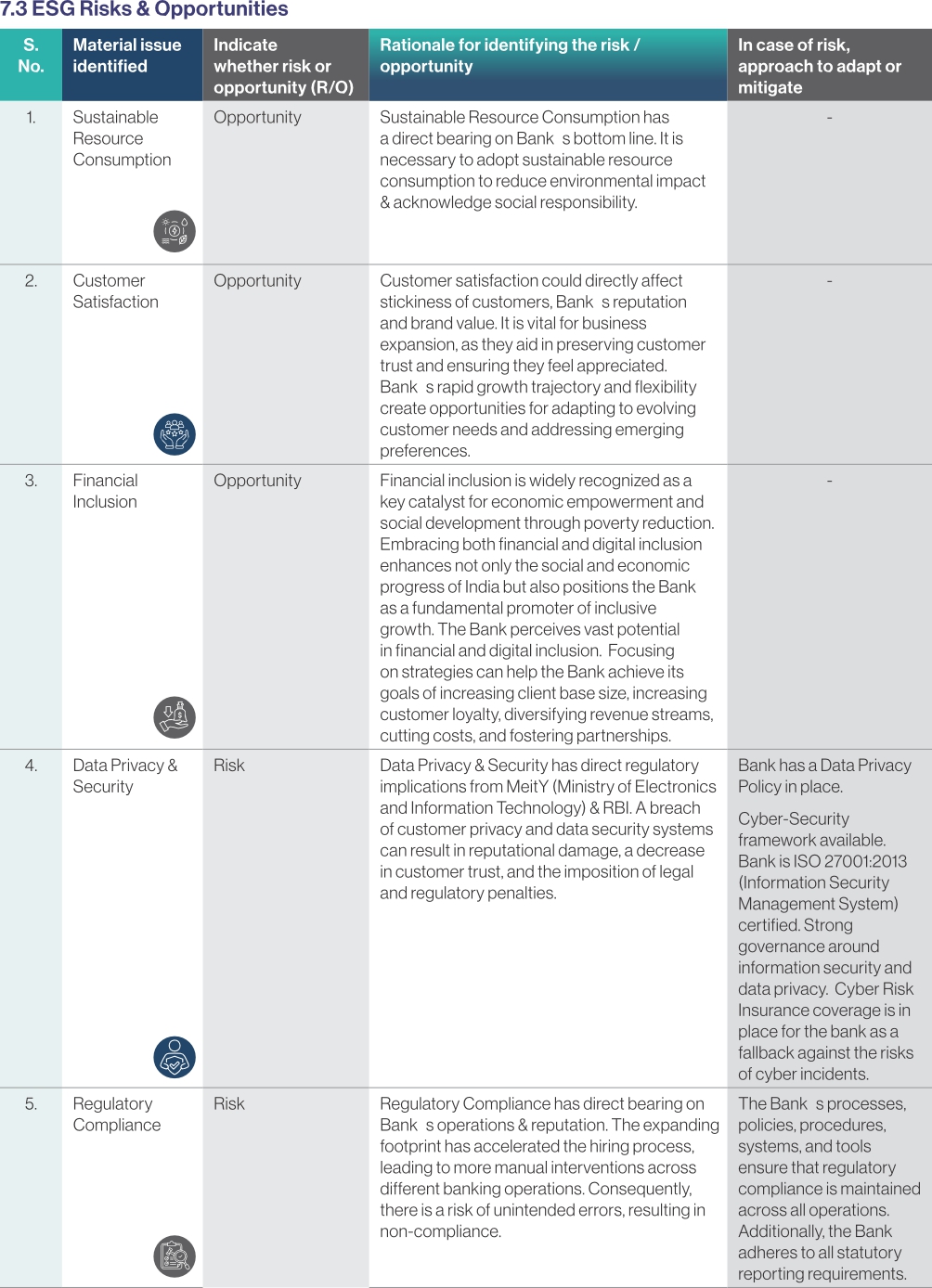

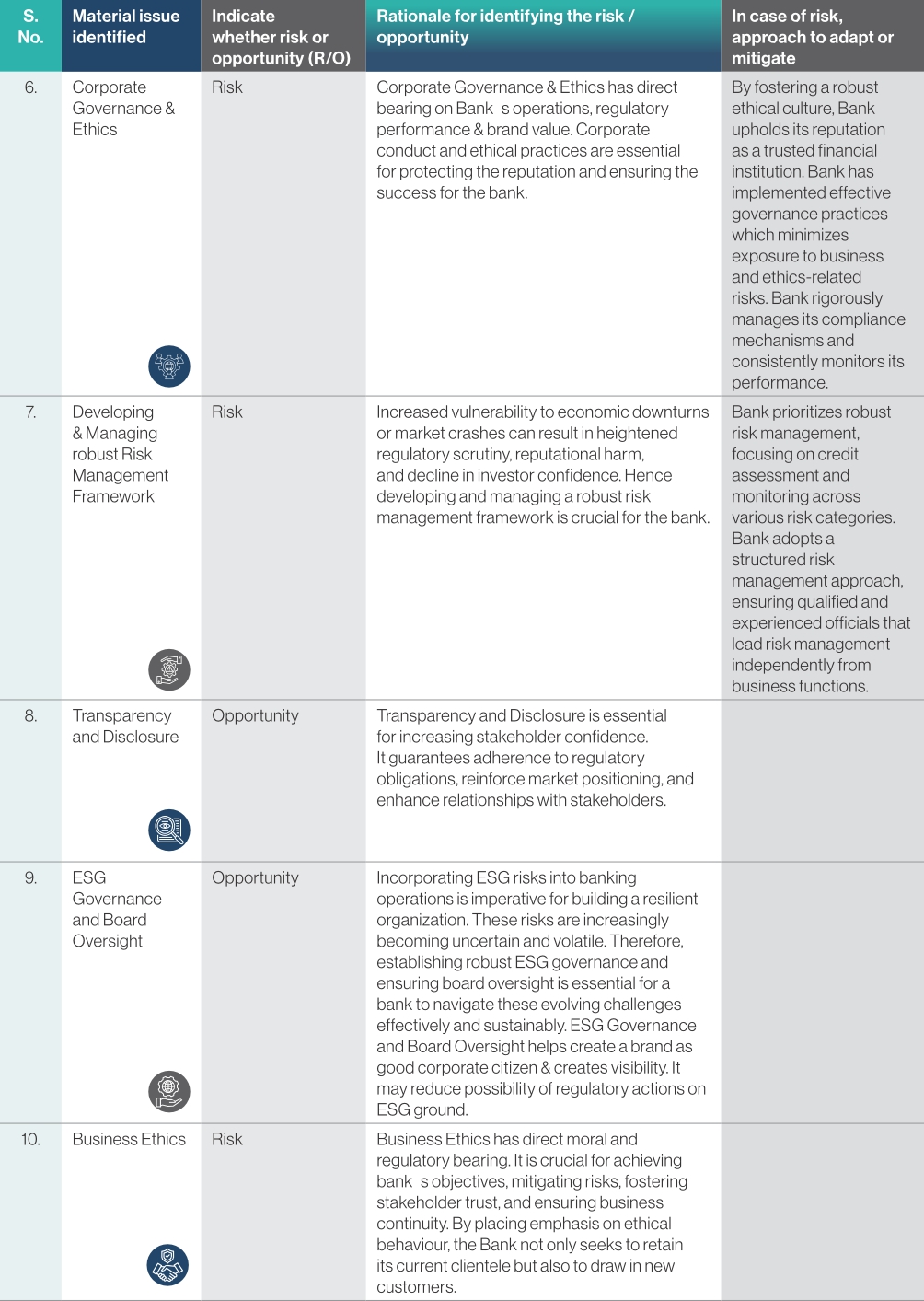

ESG Risks & Opportunities

Principles of Responsible Banking (PRB) and Utkarsh Small Finance Bank

The Principles for Responsible Banking (PRB), developed by the United Nations Environment Programme Finance Initiative (UNEP FI) in collaboration with 30 founding banks, came into force on 22 September 2019 at the UN General Assembly in New York. On that date, more than 130 banks from 49 countries, collectively representing over USD 47 trillion in assets, became the first official signatories to the principles.

The Principle of Responsible Banking (PRB) was established to align the strategies and practices of the banking sector with society’s evolving needs particularly in environmental, social, and governance

(ESG) areas to advance the global goals embedded in the UN Sustainable Development Goals (SDGs) and the Paris Climate Agreement, while also considering regional and national development priorities. These principles encourage

banks to play a pivotal role in addressing global challenges such as climate change, biodiversity loss, inequality, and social inclusion.The framework emphasizes that banks should align their business strategies

with global and local sustainability goals to ensure that long-term growth is balanced with responsibility towardpeople and the planet. They are expected to continuously assess the environmental and social impacts of their

financing activities and, based on these assessments, set clear targets to address their most significant impacts.

Such targets may relate to climate action, biodiversity conservation, financial inclusion, or the protection of human rights, and they should be publicly disclosed to enhance credibility and accountability

In addition, banks are encouraged to work with their clients and customers to foster sustainable practices, providing products and services that enable a shift toward greener and more inclusive economic models. This

collaboration is complemented by the need to engage with a wide range of stakeholders, including regulators, investors, civil society, and local communities, to drive collective progress toward sustainable development.

Effective implementation of these principles also relies on embedding strong governance mechanisms and fostering a culture of accountability throughout the organization. This requires integrating sustainability

into decision-making processes, risk management, incentive structures, and employee training. Finally, transparency and accountability are central to the framework, with banks committing to regularly disclose their progress,

challenges, and achievements in implementing the principles. This openness not only builds trust but also ensures continuous improvement

in the sector’s contribution to global sustainability.Utkarsh Small Finance Bank (USFB) has been founded on the mission of financial inclusion, with the vision to empower underserved communities

through access to affordable credit, savings, and other financial services. As a progressive institution committed to sustainable growth, the Bank recognizes that its long-term success is inherently tied to the prosperity of

the environment, society, and economy in which it operates.

By aligning with the UN Principles for Responsible Banking (PRB), Utkarsh

Small Finance Bank reaffirms its dedication to embedding sustainability at the core of its business strategy, operations, and stakeholder engagement. The PRB framework provides a comprehensive guide to shaping

a resilient banking system that contributes to people’s needs and societal goals as expressed in the Sustainable Development Goals (SDGs) and the Paris Climate Agreement.The following sections highlight how Utkarsh Small

Finance Bank is embracing each principle of responsible banking, while continuing to strengthen its position as a purpose-driven institution

Principle 5: Governance & Culture

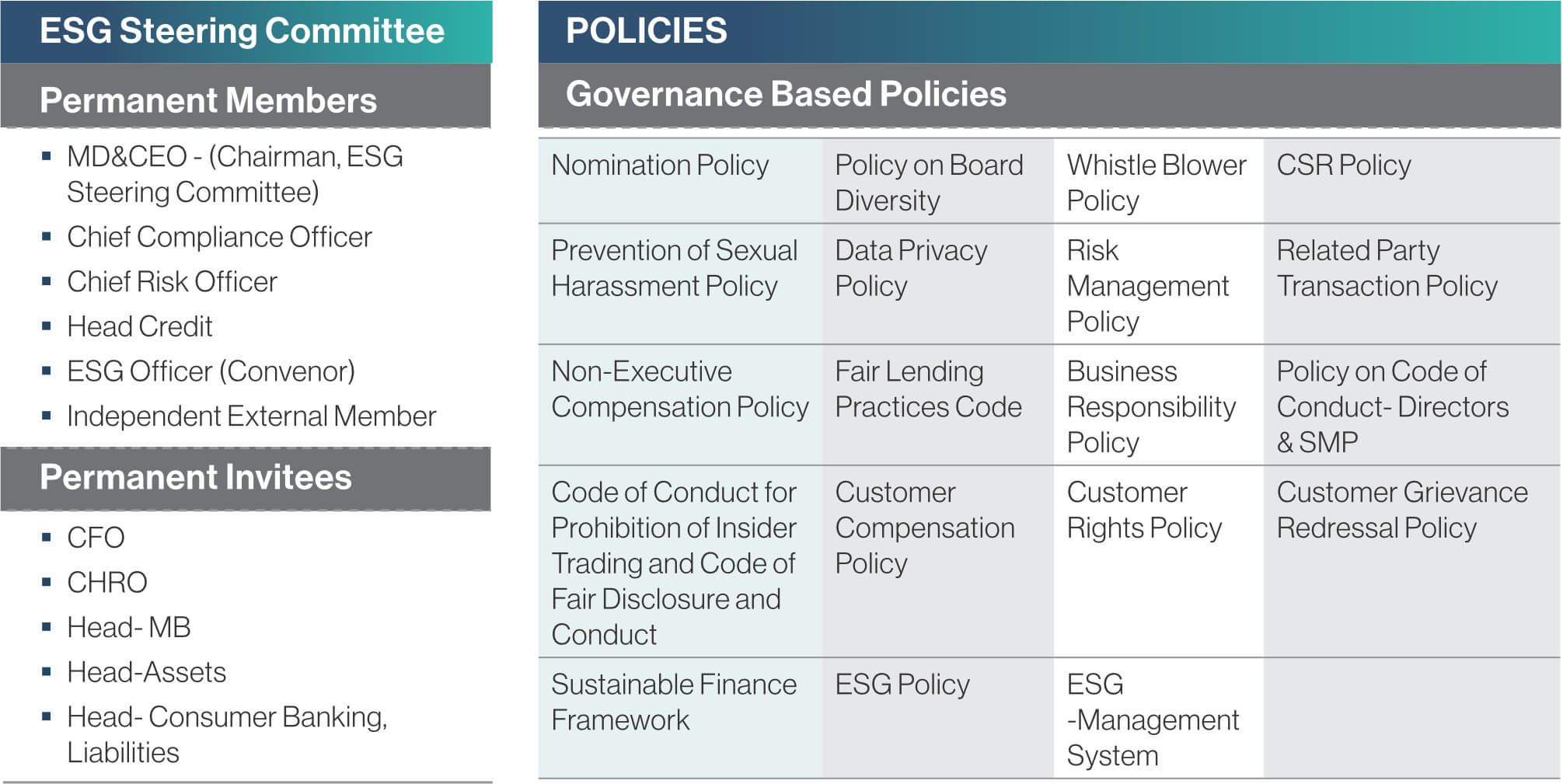

We implement our commitment to these Principles through effective governance and a culture of responsible banking. Governance forms the backbone of responsible banking. At Utkarsh, we ensure that sustainability considerations are integrated into our governance framework and decision-making processes: Management Level Oversight: The Bank’s ESG Steering Committee monitors environmental, social, and governance (ESG) performance. Policies & Frameworks: Implementation of ESG policies, ethical lending standards, and Sustainable Finance Framework.Culture of Responsibility: Internal training programs for employees to foster awareness of sustainability practices, customer ethics, and financial responsibility.Diversity & Inclusion in Governance: Representation of women and professionals from varied backgrounds in senior management positions This culture of responsibility ensures that our workforce is aligned with the values of integrity, transparency, and accountability.

Contribution to SDGs

Utkarsh SFB strives to balance financial success with social responsibility and environmental stewardship. Its sustainability strategy outlines a clear roadmap, ensuring that its operations are in step with current ESG trends, regulatory requirements, and stakeholder expectations. By embedding sustainable banking practices, the bank strengthens the adaptability of the financial system, tackles pressing environmental and social issues, and supports the transition to a more sustainable and inclusive economy.

- Financial Inclusion for Positive Social Impact

- Addressing the Financial Divide

- Our Rationale for Existence

- Customer Centricity and Service Innovation

- Customer Satisfaction and Grievance Management

Financial Inclusion for Positive Social Impact

Financial inclusion is not just a service; it’s a fundamental right and a prerequisite for the well-being of individuals and the cohesion of society.

Addressing the Financial Divide

We are passionate about setting up a new age lending entity leveraging technology to bring about a positive change in lives of the underserved segment of India. The Company focuses on reaching out to unbanked and providing financial services to women entrepreneurs. Along with financial services, we also shoulder the responsibility of educating our clients on financial literacy. This holistic approach contributes to empowering women entrepreneurs, fostering economic independence and promoting financial well-being in rural communities.

By providing financial services to the underserved, we contribute to SDG 1 (No Poverty), addressing economic disparities. Our commitment to supporting women entrepreneurs aligns with SDG 5 (Gender Equality), fostering empowerment in rural communities. Embracing technology for financial inclusion reflects alignment with SDG 9 (Industry, Innovation, and Infrastructure). The mission to reduce inequalities in access to financial services corresponds to SDG 10 (Reduced Inequalities), promoting inclusive growth. Our Collaborative efforts in financial literacy and partnerships contribute to SDG 17 (Partnerships for the Goals), emphasizing the importance of collective action for sustainable development. We are dedicated to create a positive social impact and align with the global agenda for a more equitable and sustainable future.

Our Rationale for Existence

We empower low-income individuals and micro-entrepreneurs by giving them access to formal financial services.

At the heart of Utkarsh’s journey lies a deep commitment to financial inclusion, which forms the foundation of its very rationale for existence. The institution was established with a vision to bridge the gap between mainstream financial services and the millions of underserved individuals across India, especially in semi-urban and rural geographies. For far too long, these communities have remained excluded from formal banking systems, relying instead on informal credit sources that often trap them in cycles of debt. Utkarsh recognises that the ability to access credit, savings, and other financial services is not merely a matter of convenience but a fundamental enabler

of economic empowerment and social transformation.

One of the most significant aspects of Utkarsh’s financial inclusion strategy is its focused attention on women entrepreneurs. Globally, evidence shows that women are disproportionately excluded from formal finance despite being central to household welfare and community development. Through our comprehensive approach, we serve over 30 lakh women customers, most of whom are microfinance borrowers organised through self-help groups and joint liability groups. By extending microfinance loans, encouraging entrepreneurship, and embedding financial literacy programs, Utkarsh

provides women with tools to not only enhance their income but also improve decision-making power within families.

On Ground Capabilities

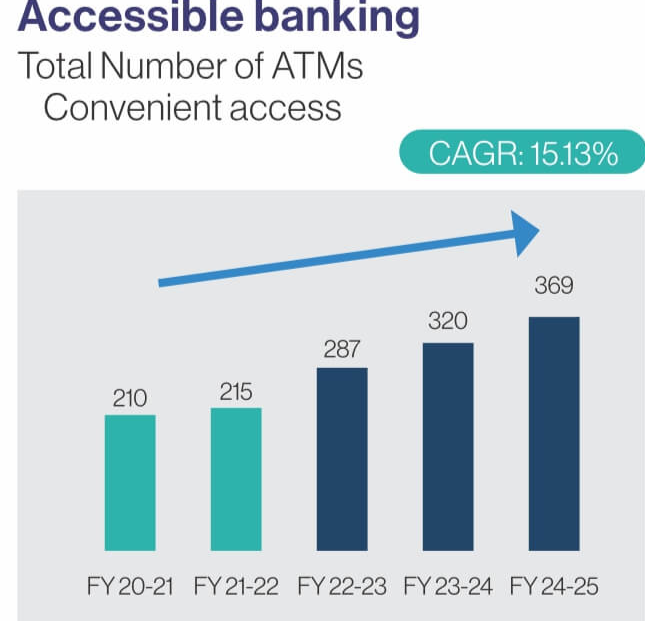

Accessibility to savings and transactional banking is equally vital in financial inclusion. Utkarsh has recognised that reaching underserved communities requires not only offering credit but also facilitating deposits, withdrawals, and remittances. To this end, the bank has expanded its ATM network steadily at a CAGR of 15%, achieving a total of 369 ATMs as of the end of March’25. Our Branch network has been growing to 1092 at a CAGR of 18% in 27 states of the country.

Geographically, our presence reflects our commitment to reaching the most underserved regions. Nearly 86 percent of our micro-banking branches are located in rural and semi-urban locations, ensuring that financial inclusion is not limited to cities but reaches the heart of India’s villages. By placing our branches closer to communities that need them most, we make it easier for individuals to access savings accounts, loans, insurance, and other essential services without having to travel long distances. This local presence also helps build trust, as

customers engage with staff who often come from the same regions and understand their circumstances deeply.

This growing network allows customers in remote areas to access their funds with ease and enabling greater financial independence. The accessibility of ATMs, coupled with digital banking initiatives, helps bridge the gap between rural customers and the modern financial system, reducing the friction of financial transactions

Borrowers

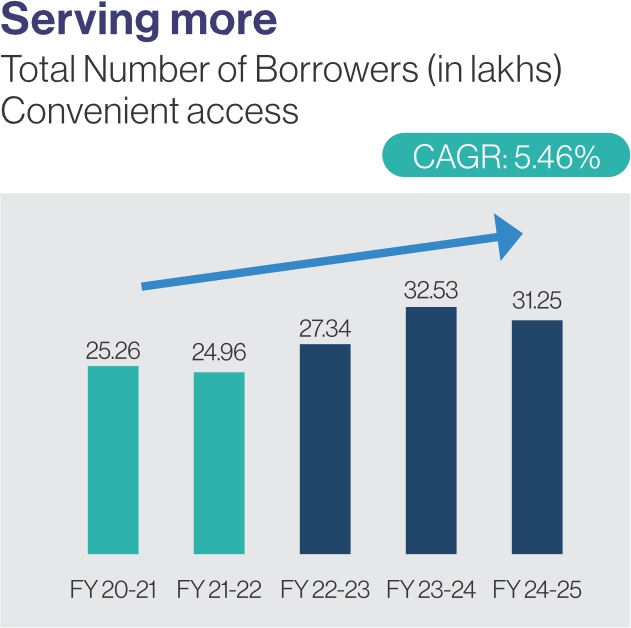

As of 31st March’25, Utkarsh serves over 31 lakh borrowers, reflecting the magnitude of its reach and impact. This vast borrower base represents more than just numbers; it embodies stories of transformation from small farmers investing in better seeds and equipment, to artisans scaling up their traditional crafts, to women establishing small businesses that support household income. Every borrower connected to the Utkarsh ecosystem demonstrates the institution’s ability to convert vision into action.

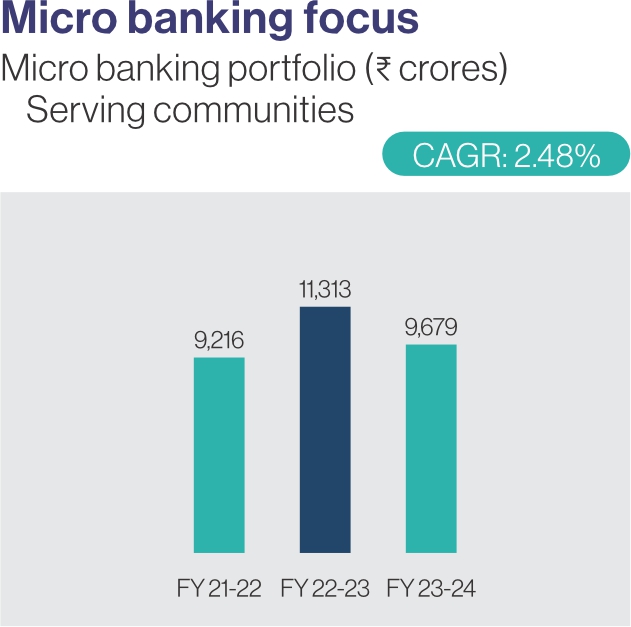

Loan Book

The bank’s loan book growth further highlights this commitment. Micro banking, which accounts for 49% of the total loan portfolio and stands at ₹9,679 crores, underscores Utkarsh’s foundational focus on serving the most vulnerable. Micro-loans are often modest in size but high in impact, enabling clients to invest in livestock, expand local shops, or purchase tools necessary for their trade. Such small-ticket loans fuel big dreams, proving that financial inclusion is not about charity but about enabling resilience and economic participation

Housing Finance

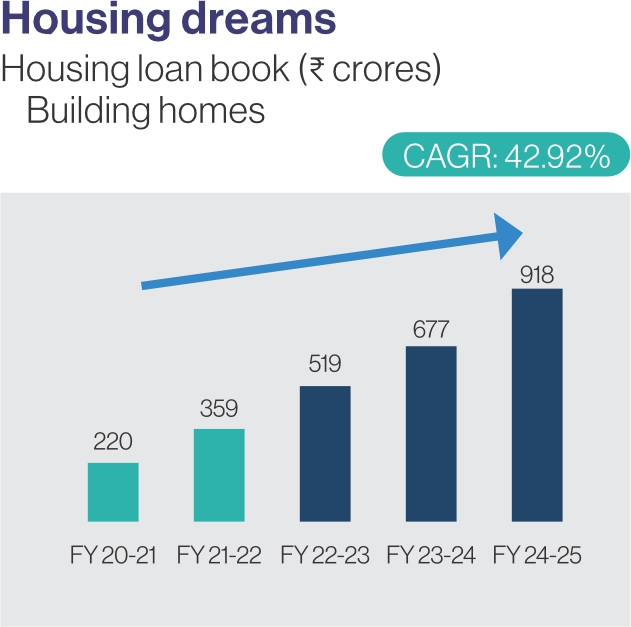

Recognising that secure shelter is a cornerstone of dignity and stability. The housing loan portfolio, which has grown at a compound annual growth rate of 42.92% to reach ₹918 crores, enables families in underserved markets to own or upgrade their homes. This not only strengthens household well-being but also contributes to community stability and local economic growth through increased demand for constructionrelated services

Microfinance

Our microfinance portfolio with more than 30 lakh borrowers, represents one of the largest networks of women-led borrowing groups in the country. These groups are not only financial collectives but also platforms for peer learning, solidarity, and social change. Women who once had no access to credit now run small businesses, from tailoring and handicrafts to vegetable vending and dairy farming creating steady income streams that uplift their families. The multiplier effect of empowering women is visible across dimensions—better nutrition and education for children, improved health outcomes, and a stronger social fabric in communities

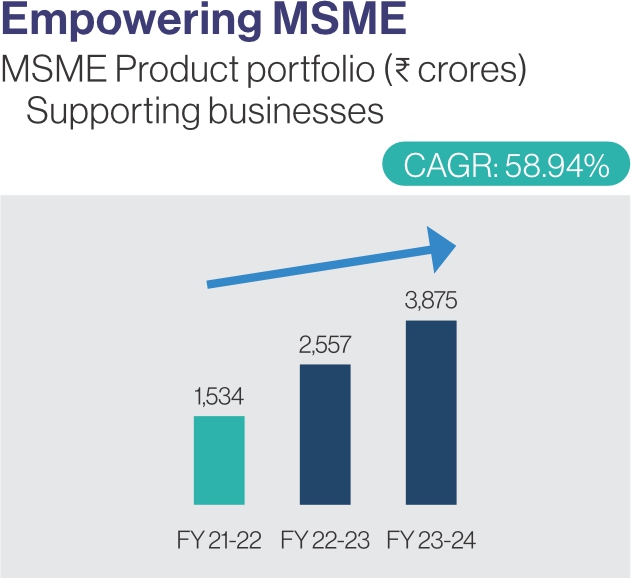

MSME Lending

Supporting micro, small and medium enterprises with tailored financial products enables business growth and job creation in underserved markets.MSME lending has been growing at an impressive CAGR of 59%.

Empowering MSME

MSME Product portfolio (₹ crores) – Supporting businesses

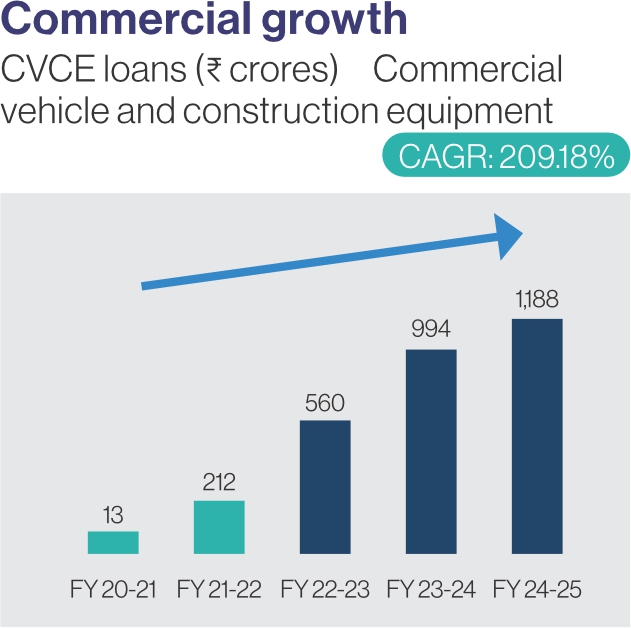

Commercial Vehicle and Construction Equipment (CVCE) Financing

Providing entrepreneurs with access to commercial vehicles and construction equipment, enabling them to expand their businesses and increase income potential. CVCE Financing has been growing fast and has reached ₹1,188 Crores.

Financial Literacy

Financial literacy remains a critical enabler of true financial inclusion, which Utkarsh has embedded this into its model. Providing access to financial products is not enough; communities must also be equipped with the knowledge and confidence to use them effectively. Through structured training sessions, community meetings, and awareness programs, the bank empowers customers to make informed decisions about savings, credit, and investments. This ensures that financial inclusion translates into long-term, sustainable growth for individuals and communities rather than short-lived access.

Impact

The impact of our financial inclusion efforts is visible in stories from across rural India. A woman in Bihar who once borrowed to purchase a sewing machine now runs a tailoring business that supports her family and pays for her children’s education. A group of women in Uttar Pradesh have pooled their microfinance loans to start a dairy enterprise that supplies milk to local markets. Farmers in Madhya Pradesh use agricultural loans to invest in better seeds and equipment, improving productivity and incomes. These stories illustrate how financial services, when accessible and inclusive, become powerful tools of transformation.

The broader mission of Utkarsh is to foster economic independence and promote inclusive, sustainable growth across rural India. By addressing the unique needs of rural populations—whether through microloans, housing finance, ATMs, or literacy programs—the institution demonstrates that financial inclusion is not a side activity but the very core of its strategy. It views every borrower, depositor, and entrepreneur not just as a customer but as a partner in the collective journey of economic empowerment.

In conclusion, Utkarsh’s commitment to financial inclusion goes beyond banking—it is about nation-building at the grassroots. Every loan disbursed, every ATM installed, and every literacy workshop conducted contributes to strengthening the financial fabric of the country. As India continues its journey towards becoming a more equitable and prosperous society, institutions like Utkarsh will play a pivotal role in ensuring that no community is left behind. The story of Utkarsh is thus not only about business growth but also about social transformation, demonstrating how financial services can be a powerful instrument for inclusive and sustainable development.

Customer Centricity and Service Innovation

At Utkarsh Small Finance Bank we place our customers at the heart of everything we do. Our purpose goes beyond offering financial products. We aim to create meaningful experiences that make banking simple, accessible, and empowering for every individual. Customer centricity for us means listening carefully to customer needs, designing solutions that address those needs, and continuously innovating to improve convenience, reliability, and trust.

A central part of our approach is the use of digital technology to bring services closer to customers. We have embraced paperless banking as a way to reduce our environmental footprint while also simplifying customer interactions. These changes make account opening, loan processing, and other services faster and more transparent for customers,

many of whom are first-time users of formal banking

We have also invested in digital platforms that improve financial literacy and inclusion. By integrating education with access, we ensure that customers not only use banking services but also understand them, thereby reducing the risks of misuse or financial vulnerability

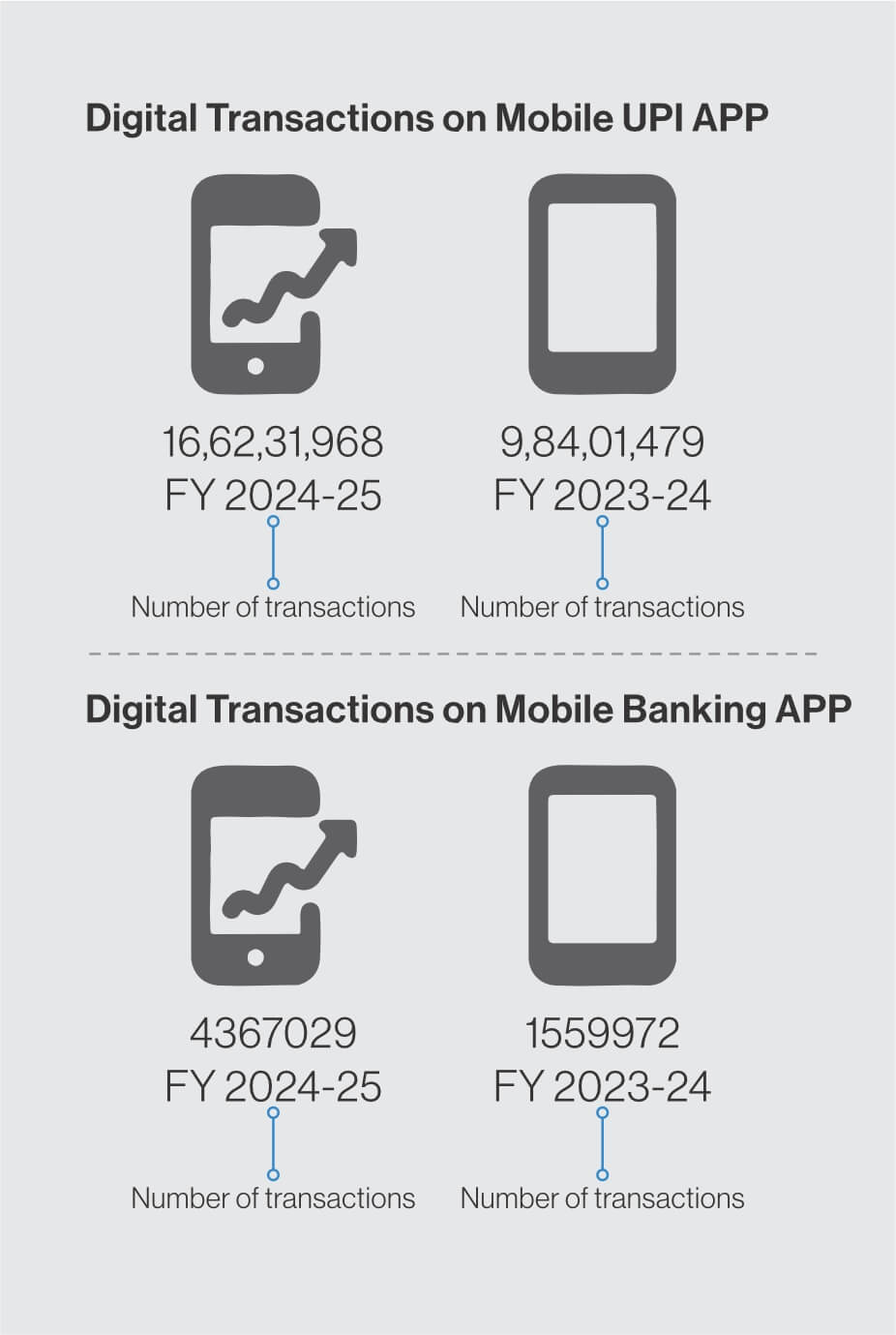

The growth in mobile and UPI transactions highlights how our innovations are being embraced by customers. We also recognize that many of our customers face challenges such as limited literacy, language barriers, or lack of familiarity with technology. This ensures that customers can interact with us in the language they are most comfortable with, enhancing both accessibility and trust. We have also introduced innovative tools such as QR-enabled kiosks, AI-driven chatbots, and video KYC facilities. These tools not only reduce the time taken for services but also empower customers to manage

their financial activities independently and securely.

Customer centricity is not only about digital solutions. It is also about ensuring that the personal touch remains intact. Our employees are trained to provide empathetic and patient support, especially to first-time customers. We encourage our staff to view every interaction as an opportunity to build confidence and trust. In communities where formal banking is a new experience, this human-centred approach makes all the difference in creating lasting relationships.

Through our customer centricity and service innovation initiatives we reaffirm that banking is not only about transactions but about creating long-term relationships built on trust, simplicity, and value. Our customers are our partners in growth, and every innovation we introduce is guided by the goal of making their journey with Utkarsh smoother, safer, and more rewarding.

Customer Satisfaction and Grievance Management

At Utkarsh Small Finance Bank, we understand that customer satisfaction is the foundation of trust and loyalty. For us, every customer interaction is an opportunity to reinforce this trust by delivering timely, transparent, and empathetic service. We know that banking is deeply personal for our customers, many of whom are engaging with formal financial institutions for the first time, and we are committed to ensuring that their experiences with us are smooth, fair, and respectful.

A key part of building satisfaction is listening carefully to our customers. We have developed a comprehensive grievance redressal mechanism that provides multiple channels for customers to register their concerns. Complaints can be submitted through our branches, contact centres, customer care, email, website, or the online dispute resolution portal. We have also introduced a missed call facility with a 24-hour call-back service in regional languages so that even customers with limited literacy or digital familiarity can access support. This multi-channel approach ensures that no customer is excluded and that every voice has a platform

Our grievance redressal framework is structured with a three-tier escalation system. At the first level complaints are addressed at the branch itself, where staff members are empowered to

provide quick solutions. If issues remain unresolved, they are escalated to the Nodal Officer, and finally, if needed, to the Principal Nodal Officer. This structure ensures accountability at each level while maintaining a clear timeline for resolution. For normal cases we aim to resolve complaints within ten working days, with specific timelines applied to complex issues. By setting clear standards we ensure that grievances are not only addressed but addressed promptly.

Customer satisfaction is also measured and monitored through regular surveys and audits. We conduct structured customer satisfaction surveys, branch audits, and analytics-based reviews of service quality. These exercises help us identify areas of strength and highlight opportunities for improvement. We were able to improve complaint resolution speed by nine percent year-on-year, demonstrating measurable progress in our responsiveness.

The combination of surveys, audits, and grievance mechanisms creates a feedback loop that continuously strengthens our services. Every grievance resolved is not just a problem addressed but also a learning opportunity. We use these insights to refine our policies, simplify processes, and train our employees, ensuring that similar issues do not recur. This commitment to learning from our customers is what allows us to evolve as an institution that truly reflects the needs of the people we serve

- ESG Policy

- Incorporating Environmental and Social Considerations into Lending Practices

- Sustainable Finance Framework

- Energy Management

- Climate Change Strategy, Risk and Transition

- Paris Climate Agreement

- RBI Draft Disclosure on Climate Risks (2024)

- Climate Roadmap

- GHG Emissions & Net Zero Target

- Water Management

- Digitisation and Sustainable Resource Consumption

- Resource Efficiency & Waste Management

- Green Building and Sustainability Initiatives

ESG Policy

As a financial institution dedicated to sustainable development, Utkarsh Small Finance Bank acknowledges that enabling progress entails safeguarding the shared environment. While the Bank’s core operations are not typically resource-intensive, its extensive footprint, comprising 1092 branches across 27 States and Union territories along with a growing digital infrastructure, inevitably creates environmental impacts. These impacts stem from energy use, branch operations, water consumption, and financed emissions linked to the lending portfolio. The Bank therefore pursues an environmental strategy focused on reducing direct emissions, enhancing resource efficiency, and supporting the transition to a low-carbon economy.

Utkarsh Small Finance Bank is committed to enhancing its positive

environmental impact throughout its business activities and operations. This commitment is reflected in the integration of sustainability into daily practices, coupled with a structured approach to accelerate the adoption of targeted initiatives. The Bank has taken tangible steps towards greener operations, including the construction of its GRIHA 5-star rated headquarters, Utkarsh Tower, which operates at 40% higher energy efficiency compared to conventional buildings.

Natural Resource efficiency is another significant agenda to the Bank’s environmental commitment. At Utkarsh Tower, water consumption has been reduced by approximately 70% through the use of efficient flow fixtures and conservation measures.

To ensure that these initiatives are implemented effectively and aligned with broader sustainability goals, oversight is provided by a board-level CSR Committee. Comprising of five independent directors and one executive director, this committee is responsible for driving the Bank’s sustainability agenda, embedding Environment, Social, and Governance (ESG) principles across decision-making processes, and ensuring compliance with regulatory frameworks as well as alignment with global standards such as the Global Reporting Initiative (GRI).

The Bank is cognizant to climate change as a critical concern that encompasses environmental, social, and financial dimensions and represents a material risk to the global economy.

Utkarsh Small Finance Bank recognizes that strong Environmental, Social, and Governance (ESG) practices are central to building a resilient financial institution. An ESG Policy enables the Bank to manage risks effectively, appeal to investors and customers who value ethical considerations, enhance corporate reputation, comply with regulatory requirements, and support long-term financial performance. By embedding ESG factors into operations, the Bank not only aligns itself with national priorities and global

Sustainable Development Goals (SDGs) but also fosters innovation in sustainable finance and demonstrates its commitment to addressing environmental and social challenges.

The policy sets out how ESG factors will be integrated into the Bank’s financial products and loan portfolio, providing guidance to Relationship and Credit teams on identifying, assessing, and mitigating ESG-related risks.

The Bank’s ESG Steering Committee oversees the effective implementation of the ESG Policy. This committee is supported by a dedicated ESG

team that collaborates with Credit, Relationship, and Internal Audit functions to apply ESG standards consistently across all business operations. Through this approach, Utkarsh acknowledges that financing certain borrower activities may give rise to ESG-related impacts and therefore requires systematic management. Left unaddressed, such impacts could translate into credit, regulatory, or reputational risks over time. Conversely, proactive ESG integration can strengthen brand differentiation, improve portfolio performance, deepen borrower relationships, and enhance long-term customer loyalty

Operational Principles

The Bank’s Environmental and Social (E&S) Policy is underpinned by a set of operational principles designed to guide ESG performance across lending and business operations:

1. Preventing Pollution & Using Resources Efficiently: Promoting cleaner production, energy efficiency, and conservation of natural resources in

both the Bank’s operations and financed activities

2. Operating an E&S Management System: Implementing a structured framework for identifying, monitoring, and managing ESG risks throughout the loan lifecycle.

3. Borrower Protection: Ensuring that financing activities uphold borrower rights, avoid exploitative practices, and foster responsible lending

4. Ensuring Good Working Conditions and Fair Labour Practices: Supporting decent work, non-discrimination, fair wages, and safe working environments in alignment with national labour laws and global standards.

5. Engaging with Stakeholders and Access to Remedy: Maintaining open channels of communication with stakeholders, addressing grievances transparently, and providing mechanisms for remedy where necessary.

Implementation & Applicability

The ESG Policy and its guiding principles have been formally adopted by the Board of Directors of Utkarsh Small Finance Bank. The policy applies to all loans disbursed by the Bank from the date of approval onwards, ensuring consistency and accountability across the entire lending portfolio. Implementation is supported by the Bank’s Environmental, Social & Governance Management System (ESGMS), which provides the framework for operationalizing the policy at every stage of financial decision-making.

Communication, Support & Training

To ensure organization-wide alignment, the ESG Policy and its associated principles have been communicated to employees through structured training and awareness programs. These programs build internal capacity,

enabling relationship and credit teams to apply ESG considerations during credit appraisal and monitoring. In addition to internal communication, the Bank has shared its ESG Policy with relevant external stakeholders, including investors and borrowers, and made the document publicly accessible on the Bank’s website. This ensures transparency and strengthens stakeholder trust

Review & Updates

Recognizing the dynamic nature of ESG risks and regulatory requirements, the ESG Policy is subject to periodic review and revision to ensure its continued relevance and effectiveness. At a minimum, the policy will undergo review every three years, though updates may be undertaken sooner if necessitated by evolving environmental, social, or governance contexts. This commitment ensures that the Bank remains responsive to changing stakeholder expectations

and aligned with best practices in sustainable finance

Audit & Compliance

To uphold accountability and transparency, the ESG Policy and its implementation are subject to regular oversight through the Bank’s established Internal Audit framework. Internal Audit will assess adherence to ESG requirements, identify areas for improvement, and provide assurance to the Board and Senior Management regarding the effectiveness of ESG integration. These audits serve as an essential feedback mechanism, ensuring that ESG commitments translate into consistent on-the-ground practices and outcomes.

The Bank’s ESG Policy, accessible at Utkarsh ESG Policy, reflects a long term commitment to embedding sustainability in financial operations and to managing risks in a manner that promotes resilience, responsibility, and value creation for all stakeholders.

Incorporating Environmental and Social Considerations into Lending Practices

ESG Integration in Lending

Incorporating Environmental, Social, and Governance (ESG) considerations into lending practices is becoming increasingly important for financial institutions. As stakeholders demand greater accountability, banks are expected to evaluate not only the financial viability of borrowers but also the potential environmental and social impacts of their activities. Utkarsh Small Finance Bank has established an Environment and Social Risk Management System (ESMS) aligned with its Environment and Social Policy. This system helps identify, assess, and mitigate risks associated with lending, thereby ensuring that financial growth is achieved responsibly while safeguarding the environment and communities.

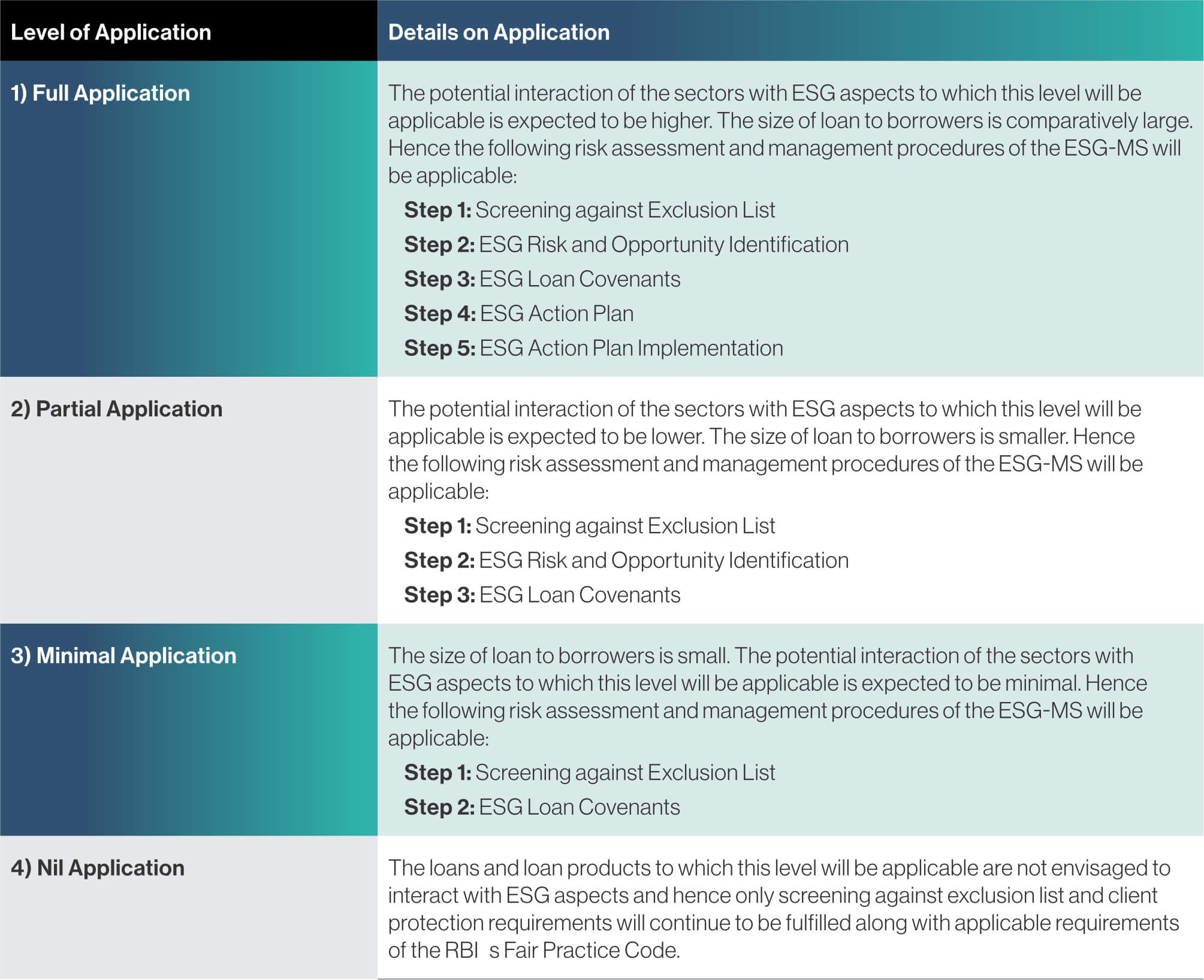

Applicability of ESGMS to Loan Products

The ESGMS (ESG Management System) framework is not uniformly applicable across all loan products. Its applicability varies depending on the nature of the business, sectoral exposure, and the degree of interaction with ESG aspects. For instance, projects in sectors with higher environmental footprints, such as infrastructure or manufacturing, undergo rigorous ESG assessments compared to low-risk

segments like retail loans. This ensures proportional application of ESG safeguards, optimizing resources while maintaining effective oversight.

Levels of ESGMS Application

The Bank applies ESGMS (ESG Management System) at different levels based on the intensity of environmental and social risks. At the basic level, standard screening is applied to identify borrowers operating in excluded or restricted sectors. At

the intermediate level, enhanced due diligence is conducted for sectors with moderate risks, where compliance with national regulations and sectoral standards is verified. At the advanced level, comprehensive environmental and social risk assessments are carried out for high-risk sectors, incorporating monitoring mechanisms and corrective action plans. This tiered approach ensures that ESG due diligence remains both robust and practical.

The level of ESGMS application is differentiated across loan categories. Retail loans, such as personal or housing loans, fall under the basic level due to their limited environmental and social implications. Loans to micro, small, and medium enterprises (MSMEs) are

assessed at the intermediate level, as these businesses may have moderate sectoral risks. Large corporate loans and project finance, especially in sectors like energy, infrastructure, and heavy manufacturing, are subjected to advanced ESGMS assessments due to

their significant environmental and social footprints. This categorization ensures that ESG principles are embedded in lending practices while maintaining balance between financial inclusion and sustainability.

Sustainable Finance Framework

The Reserve Bank of India (RBI) joined the Central Banks and Supervisors Network for Greening the Financial

System (NGFS) as a Member on April 23, 2021.

Launched at the Paris One Planet Summit on December 12, 2017, the NGFS is a group of central banks and supervisors willing to share

best practices and contribute to the development of environment and climate risk management in the financial sector, while mobilising mainstream finance to support the transition towards a sustainable economy.

Subsequent to joining the (NGFS) the RBI set up a sustainable finance group (SFG) within its department of regulation in May’21 to lead the regulatory initiative in the area of climate risk and sustainable finance in the Indian context.

In April 23 RBI came up with the Framework for acceptance of Green Deposits. RBI said “Climate change has been recognised as one of the

most critical challenges faced by the global society and economy in the 21st century. The financial sector can play a pivotal role in mobilizing resources and their allocation thereof in green activities/projects. Green finance is also progressively gaining traction in India. Taking this forward and with a view to fostering and developing green finance ecosystem in the country, it has been decided to put in place the enclosed

Framework for acceptance of Green Deposits for the REs”.

Considering the RBI guidance and the global developments Utkarsh Small Finance Bank Limited has adopted “Sustainable Finance Framework” in May’25. The framework provides for sustainable finance solutions in the areas of

Utkarsh’s Sustainable Finance Framework provides that the allocation of the proceeds would be done on the eligible projects in Environmental, Social and Farm Segments:

ALLOCATION OF PROCEEDS ON PROJECTS IN

Renewable Energy (including, production, transmission and distribution): This would include in solar, wind, small hydro, waste to energy, geothermal energy, bioenergy.

Energy Efficiency: Investments, expenditure and financing/ refinancing related to projects and technologies that are designed to enable energy and emissions reductions that aim to achieveenergy savings.

Clean Transportation: Investments, expenditure and financing/ refinancing related to projects aiming at developing/ manufacturing low-carbon passenger and freight transportation or related infrastructure.

Climate Change Adaptation: Investments, expenditure and financing/ refinancing related to projects including

data driven systems for monitoring and / or forecasting climate related hazards.

Sustainable Water Management: Investments, expenditure and financing/ refinancing related to projects, including, developing / manufacturing infrastructure, equipment and technology for activities that improve water quality.

Pollution Prevention and Control: Investments, expenditure and financing/ refinancing related to projects in the areas of waste management, pollution control projects approved by India’s Commission for Air Quality Management (CAQM), reduction of air emission, soil remediation, recycling etc.

Green Building: Investments, expenditure and financing/ refinancing related to projects including green

buildings certified under EDGE, BREEAM, IGBC, LEED, Green Mark, GRIHA.

Sustainable Management of Living Natural Resources and Land Use: Investments, expenditure and financing/ refinancing related to projects including Programs encouraging sustainable land use and sustainable agriculture, including climate smart agriculture which considers climate mitigation and adaptation measures

Terrestrial and Aquatic Biodiversity Conservation: Investments, expenditure and financing/ refinancing related to projects including Preserving terrestrial / marine natural habitats.

Circular Economy and/or EcoEfficient Projects: Investments, expenditure and financing/ refinancing

related to projects including, environmental and sustainability benefits of circular economy and/or eco-efficient projects, production of bio-based resource-efficient/ low carbon products that are RSB certified.

Access to Essential Services:

Investments, expenditure and financing/ refinancing related to projects including Healthcare, Education, financing.

Affordable Basic Infrastructure:

Investments, expenditure and financing/ refinancing related to projects including Water, Electricity, Transportation

Affordable Housing: Loans to individuals for purchase or construction of their houses, loans to individuals for renovation of an existing house.

Employment Generation: Investments or projects related to providing employment generation, including Loans to MSMEs as defined by the Government of India. Further, such MSMEs should be engaged in the manufacture or production of goods, in

any manner, pertaining to any industry specified in the First Schedule to the Industries.

Food Security: Investments or projects related to Investment in infrastructure and facilities such as warehouses to provide adequate storage, improve food conservation or improve connectivity in the food chain to avoid food losses.

Farm Credit: Investments or projects related to enabling socio-economic advancement and empowerment, including lending to the agriculture sector shall include Farm Credit short term crop loans and medium/long term credit to farmers, and ancillary activities.

Agriculture Infrastructure: Loans to self-help groups (SHGs) or Joint Liability Groups (JLGs) i.e. Group of Farmers, Small/Marginal Farmers, Farmer Cooperatives of Small/marginal Farmers Directly engaged in Agriculture and Allied Activities, viz., dairy, fishery, animal husbandry, poultry, bee-keeping and sericulture. It includes crop loans to

farmers, which shall include traditional/non-traditional plantations and horticulture, and loans for allied activities

Ancillary Activities: Loans up to ₹5 crore to co-operative societies of farmers for disposing of the produce of members, loans for setting up of agri-clinics and agri-business centers, bank loans to Primary Agricultural Credit Societies (PACS), Farmers’ Service Societies (FSS) and Large-sized Adivasi Multi-Purpose Societies (LAMPS) for on lending to agriculture.

Socio-Economic Advancement and Empowerment: Loans to individual farmers, Self Help Groups (SHGs) or Joint Liability Groups (JLGs) and/or corporate farmers, producer organisations, partnership firms & Cooperatives of farmers limited to Small/Marginal farmers for soil conservation and watershed development, plant tissue culture and agri-biotechnology, seed production, production of biopesticides, bio-fertilizer, and vermi composting.

Energy Management

Energy Efficiency & Conservation Strategy

Utkarsh recognises that its business operations, while primarily serviceoriented, contribute to direct and indirect emissions through electricity consumption, diesel generator usage, and operations of company-owned vehicles. Energy conservation is therefore positioned as both an environmental necessity and a strategic imperative. With a large network of branches, offices, and data centres, cumulative energy demand is significant. By adopting energyefficient technologies and conservation practices, the Bank reduces operating

costs, enhances efficiency, and strengthens long-term profitability while supporting its commitment to the Sustainable Development Goals (SDGs), particularly those focused on clean energy and climate action.

The Bank’s energy strategy also reflects evolving regulatory frameworks that increasingly emphasise environmental performance and disclosure requirements. By proactively integrating energy efficiency into operations, Utkarsh is well-positioned to meet ESG reporting standards and stakeholder expectations. Beyond compliance, the Bank recognises that responsible energy management enhances its reputation, builds stakeholder trust, and

reinforces its leadership in sustainable business practices.

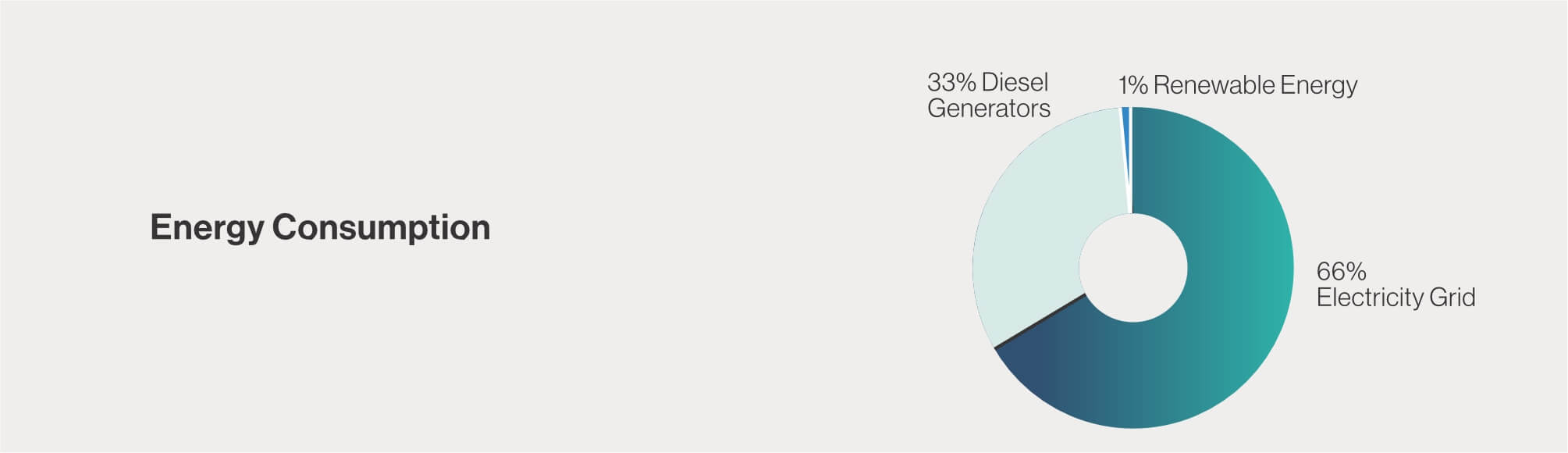

Energy Consumption (Grid, DG, Renewable)

For FY2024-25, total energy consumption amounted to 71,046 GJ, with 66% sourced from the electricity grid and 33% from diesel generators. Renewable energy contributed 593 GJ, representing an important step in diversifying the Bank’s energy portfolio towards cleaner sources. This represents the first year in which the Bank comprehensively calculated energy consumption across all branches and ATMs, establishing a robust baseline for future tracking and improvements.

Energy Intensity & Reduction Measures

The Bank reported an energy emission intensity of 18.89 GJ per crore of turnover in FY2024-25. Through targeted optimisation measures, Utkarsh has achieved a reduction in electricity consumption across its network. These results were achieved through retrofitting lighting systems with LED solutions, improving UPS and HVAC system efficiency, and introducing energy-efficient appliances across offices and branches. Such measures not only lower operational costs but also directly contribute to the Bank’s emission reduction goals.

Energy-Efficient Infrastructure (Utkarsh Tower, Appliances)

Utkarsh Tower, the Bank’s headquarters, continues to serve as a benchmark for energy-efficient infrastructure. Certified with a GRIHA 5-star rating, the building incorporates advanced design principles that deliver 40% greater energy efficiency compared to conventional buildings. During FY2024–25, Utkarsh Tower improved its energy performance by 7%, playing a pivotal role in lowering Scope 2 emissions. Energy-efficient appliances, regular maintenance of equipment, and systematic monitoring of performance further strengthen the infrastructure’s contribution to the Bank’s sustainability agenda.

Renewable Energy Initiatives

The integration of renewable energy remains a key focus of Utkarsh’s energy management roadmap. The Bank operates a 140 KWP rooftop solar photovoltaic system at its headquarters, which contributes approximately 15% of the building’s total electricity needs. In FY2024–25, renewable energy usage was recorded at 593 GJ, with plans to expand renewable adoption across the branch network in the coming years. Utkarsh has set a forward-looking target of powering 25% of its branches with renewable energy within the next two years, underscoring its long-term ambition to achieve carbon neutrality for Scope 1 and Scope 2 emissions by 2030

Climate Change Strategy, Risk and Transition

Climate change, primarily driven by greenhouse gas emissions from human activity, has become one of the most pressing global challenges of our time. Its impacts are already visible across ecosystems, communities, and economies, and are expected to intensify further in the coming decades. Rising global temperatures have disrupted weather patterns, accelerated the melting of glaciers, and contributed to sea-level rise, while biodiversity loss and ecosystem degradation have reached critical levels. These environmental shifts are no longer distant projections but present-day realities that threaten economic stability and human well-being.

The consequences of climate change are multidimensional, complex, and

deeply interconnected. They often affect the most vulnerable populations first and most severely. Increasing frequency and intensity of extreme weather events such as prolonged droughts, erratic monsoon patterns, heatwaves, cyclones, and flash floods are straining infrastructure, damaging livelihoods, and imposing additional burdens on public health systems and social safety nets. In India, which is highly dependent on agriculture and natural resources, the risks are particularly acute. Erratic rainfall patterns and delayed monsoons have already disrupted agricultural productivity, leading to food insecurity, rural distress, and income instability for communities reliant on rain-fed farming.

To achieve the alignment with global climate change mitigation and

adaptation initiatives, Utkarsh has prioritised a strategy that focuses on both operational and portfoliolevel actions. On the operational front, the Bank is working to reduce the carbon intensity of its activities through measures such as adopting energy-efficient infrastructure, increasing renewable energy usage, digitising operations to reduce paper consumption, and improving resource efficiency across branches and offices. On the portfolio side, Utkarsh is integrating climate considerations into its lending practices, assessing financed emissions, and progressively increasing exposure to climate-aligned sectors such as renewable energy, sustainable agriculture, and green infrastructure.

Paris Climate Agreement

The Paris Climate Agreement adopted in December 2015 at the 21st Conference of the Parties (COP21) in Paris is a landmark international treaty under the United Nations Framework Convention on Climate Change (UNFCCC). Its central objective is to limit the rise in global average temperature to well below 2°C above pre-industrial levels while actively pursuing efforts to restrict it to 1.5°C. This scientifically backed target represents the threshold beyond which climate impacts would become increasingly severe and potentially irreversible. The agreement came into force on November 4, 2016, and today nearly every nation is a party to it, reflecting an unprecedented level of global consensus on climate action.

What makes the Paris Agreement distinct from earlier frameworks is its inclusive and dynamic approach. Instead of imposing uniform obligations, it allows countries to voluntarily set and update their own climate action plans known as Nationally Determined Contributions (NDCs) which are reviewed and strengthened every five years. The framework is built upon five core pillars which include mitigation, adaptation, finance, transparency, and global stocktaking, making it a comprehensive and action-oriented roadmap for a sustainable future.

Utkarsh Small Finance Bank acknowledges that climate risks pose material financial risks. In the past, events such as floods, droughts, and cyclones have adversely affected the Bank’s portfolio performance, particularly in rural and semi-urban areas where clients are more vulnerable to physical climate shocks. India has been ranked among the top ten most climate-vulnerable countries in the Global Climate Risk Index, and studies indicate that climate

change could reduce India’s agricultural income by up to 25 percent in severe scenarios. Scientific projections also suggest that the frequency and severity of such events are likely to intensify due to rising greenhouse gas emissions. As such, the Bank views climate risk as an evolving area of strategic importance and is strengthening its capacity to assess, manage, and disclose the potential long-term financial implications

In addition to green infrastructure, Utkarsh has prioritized digital transformation as part of its sustainability journey. By encouraging digital banking solutions including paperless transactions, e-statements, and digital passbooks, the Bank reduces its dependence on paper and minimizes emissions from branch visits and physical documentation while enhancing customer convenience. For Utkarsh this transition is both an operational advantage and a climate-conscious choice.

Importantly, Utkarsh’s financial inclusion mission inherently contributes to climate resilience. By extending credit to microentrepreneurs, particularly women and rural households, the Bank fosters diversified and sustainable income streams. This financial empowerment allows low-income communities to invest in adaptive solutions such as climate-resilient agricultural practices, water-efficient technologies, and disaster-resilient housing. In doing so Utkarsh not only strengthens household resilience but also safeguards its loan portfolio from climate-induced shocks. With over 70 percent of India’s rural population dependent on agriculture for livelihoods, such interventions become critical for advancing both community well-being and national climate goals.

RBI Draft Disclosure on Climate Risks (2024)

The Reserve Bank of India has recently issued the Draft Disclosure Framework on Climate-Related Financial Risks, 2024, which will become applicable from FY26. This framework represents a significant regulatory shift as it requires all Indian banks to align their disclosures with the internationally recognized guidelines of the Task Force on ClimateRelated Financial Disclosures (TCFD). The framework is designed to bring greater transparency and accountability to the way financial institutions assess, manage, and disclose climaterelated risks, ensuring that climate

considerations are embedded into the financial system in a structured manner.

The framework emphasizes two critical dimensions of climate risk that banks and regulators must address. The first is the facilitative dimension which includes capacity building, the development of ecosystems that support green financing, and the scaling up of sustainable investment flows. The second is the prudential dimension which focuses on the risk management implications of climate change, ensuring that banks integrate climate-related financial risks into their core governance and decision-making processes.

Together, these dimensions highlight the dual responsibility of banks to both enable the transition to a low-carbon economy and safeguard the resilience of the financial system.

Through these efforts, we demonstrate our readiness to align with the RBI’s draft disclosure requirements. We view this framework not merely as a compliance obligation but as an opportunity to strengthen our own resilience, enhance stakeholder confidence, and actively contribute to India’s transition towards a sustainable and climate-resilient economy.

Climate Roadmap

We are formulating strategies that operate across short, medium, and long-term horizons. In the short term, our focus is on enhancing internal capacities, building systems for data collection, and identifying climate-exposed sectors within our portfolio. In the medium term, we aim to progressively measure financed emissions, conduct climate scenario analysis, and expand disclosures on physical and transition risks. Over the long term, we envision aligning our portfolio more closely with India’s national commitments under the Paris Agreement and global net-zero pathways while continuing to support

rural and underserved communities in adopting climate-resilient practices.

To achieve this, we are putting in place robust frameworks to measure and evaluate material climate risks linked to our lending and investment operations. We are also developing the capacity to assess our portfolio performance under a range of climate scenarios. These efforts allow us to proactively implement strategies that enhance the resilience of our assets while reducing vulnerabilities, ensuring that our business model is aligned with long-term climate and sustainability goals

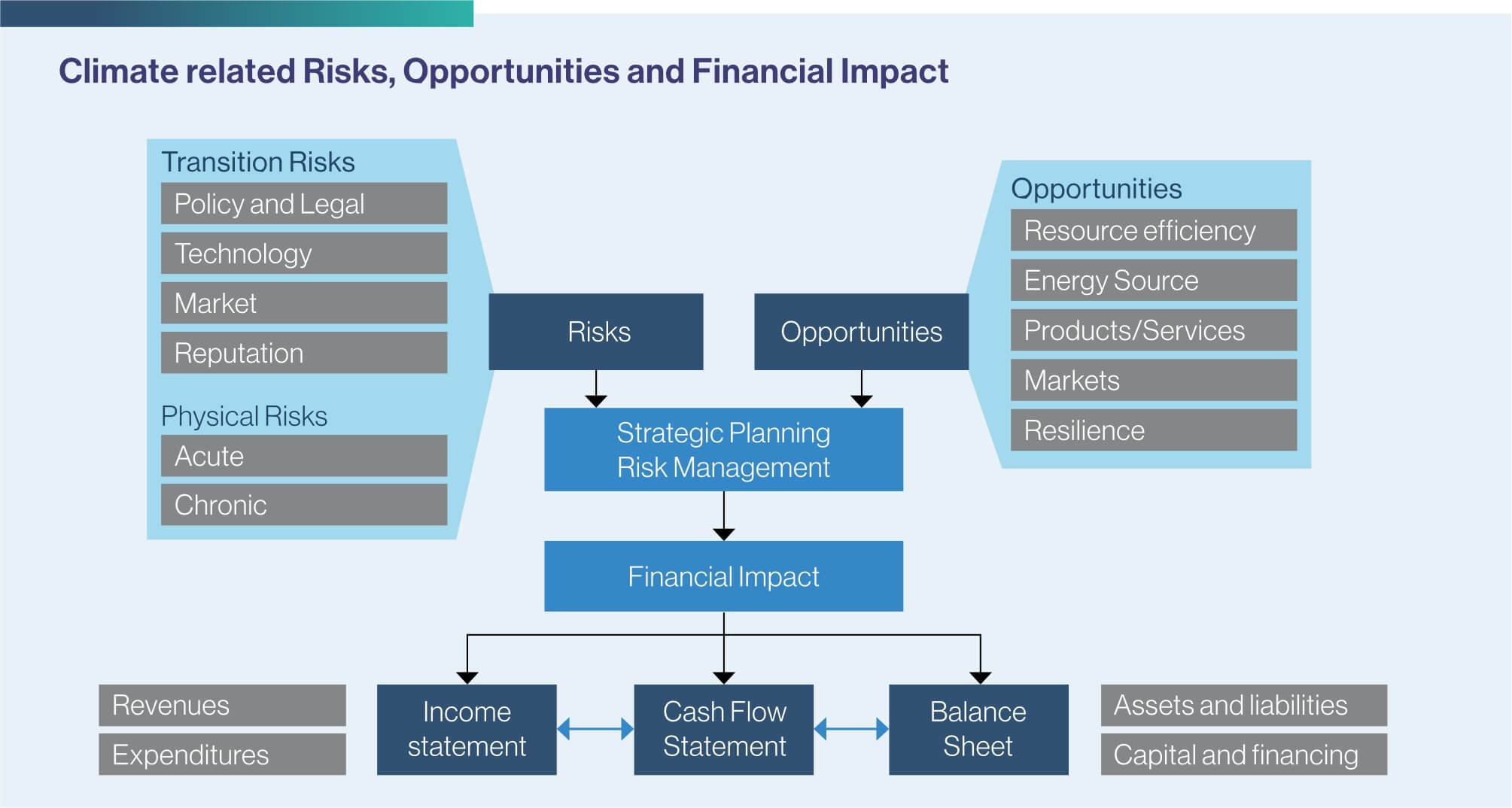

Identification of Climate-related Risks

We recognise climate change as a material financial and operational risk and have integrated it into our overall risk management architecture. Consistent with the recommendations of the Financial Stability Board’s Task Force on Climate-Related Financial Disclosures (TCFD), we view climate risk through two lenses, transition risks, which arise from the evolving policy, legal, technological, and market landscape, and physical risks, which stem from the direct impacts of extreme weather events and longterm climate shifts.

Transition Risks

Among the most significant risks we face is the tightening of disclosure policies. The global regulatory environment is evolving rapidly, with governments and supervisory bodies mandating enhanced climate and sustainability disclosures. Non-compliance with these requirements could expose organisations to penalties, legal challenges, reputational concerns, and restricted market access. We are therefore attentive not only to our own obligations but also to the challenges our clients may face. If they struggle to adapt to these new norms, their financial stability could be affected, which in turn could impact their repayment capacity and our overall portfolio quality.

Another critical dimension is the increasing stringency of environmental regulations. Across the world, new rules are being introduced that govern operating licences, occupational health and safety standards, and emission or discharge limits. While these measures are essential to safeguard people and the planet, they could increase operating costs for certain clients or, in cases of non-compliance, disrupt their ability to continue business operations. This may lead to financial stress among borrowers and potential credit risk exposure for us. To mitigate this, we have started embedding environmental risk assessments into our credit appraisal processes and continue to engage closely with our clients, supporting them in their transition towards sustainable practices.

Physical Risks

Physical risks arising from climate change also pose a significant challenge. In India, the frequency and severity of droughts, floods, cyclones, and heatwaves have increased, disrupting livelihoods and damaging assets across sectors. Agriculture and allied industries are particularly vulnerable, and since they form an important part of the economy, their fragility directly affects the financial system. Such climate events could reduce repayment capacities, disrupt operations at the community level, and affect broader economic activity. They may also impact our own operations by limiting the ability of employees to work or by affecting the physical infrastructure of our branches. These risks have wider implications

for revenue generation and long-term growth.

In response, we are enhancing our ability to stress-test loan portfolios against different climate scenarios and to anticipate the cascading effects of climate events on client performance. By engaging in dialogue with borrowers and supporting the adoption of adaptive practices, we aim to reduce vulnerability at the ground level.

Climate-related Opportunities

While climate change presents undeniable risks, it also creates opportunities for financial institutions to drive innovation, foster resilience, and accelerate sustainable growth. We view the transition to a low-carbon economy as an opportunity to diversify our portfolio, create long-term value for stakeholders, and contribute meaningfully to India’s climate and development goals

In response, we are enhancing our ability to stress-test loan portfolios against different climate scenarios and to anticipate the cascading effects of climate events on client performance. By engaging in dialogue with borrowers and supporting the adoption of adaptive practices, we aim to reduce vulnerability at the ground level.

renewable energy capacity, and we are positioning ourselves to support this transition by extending credit to solar, wind, and small hydro projects. By enabling clean energy adoption, we not only reduce exposure to high-emission sectors but also strengthen the resilience of the energy ecosystem that our clients and communities depend on.

Sustainable agriculture represents another vital area of opportunity. Given the vulnerability of Indian agriculture to climate risks, financing climatesmart solutions such as water-efficient irrigation systems, organic farming, and sustainable crop diversification practices can help farmers adapt to changing conditions. By supporting these initiatives, we simultaneously safeguard rural livelihoods and reduce the potential credit risk associated with climateinduced agricultural disruptions

We also see scope for fostering innovation in the circular economy and resource efficiency sectors. Financing businesses engaged in waste management, recycling, and sustainable packaging not only reduces

environmental pressures but also opens new growth avenues for the Bank. Similarly, encouraging clients to adopt energy-efficient technologies and green building practices aligns with both regulatory expectations and market demand.

Furthermore, climate-related opportunities extend to digital solutions that reduce environmental impact. By expanding digital banking services, the Bank reduces paper usage, cut emissions associated with physical travel, and enhance accessibility for customers. Digitalisation also improves operational efficiency, which has longterm benefits for both sustainability and financial performance

By integrating these opportunities into our business strategy, we aim to move beyond risk mitigation towards value creation. Climate-conscious financing and innovation provide us with the ability to build a future-ready portfolio that is resilient, inclusive, and aligned with global sustainability priorities.

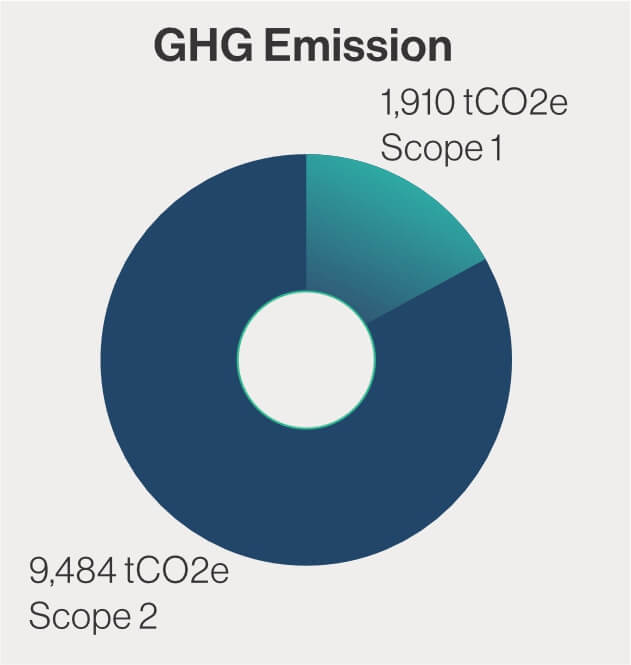

GHG Emissions & Net Zero Target

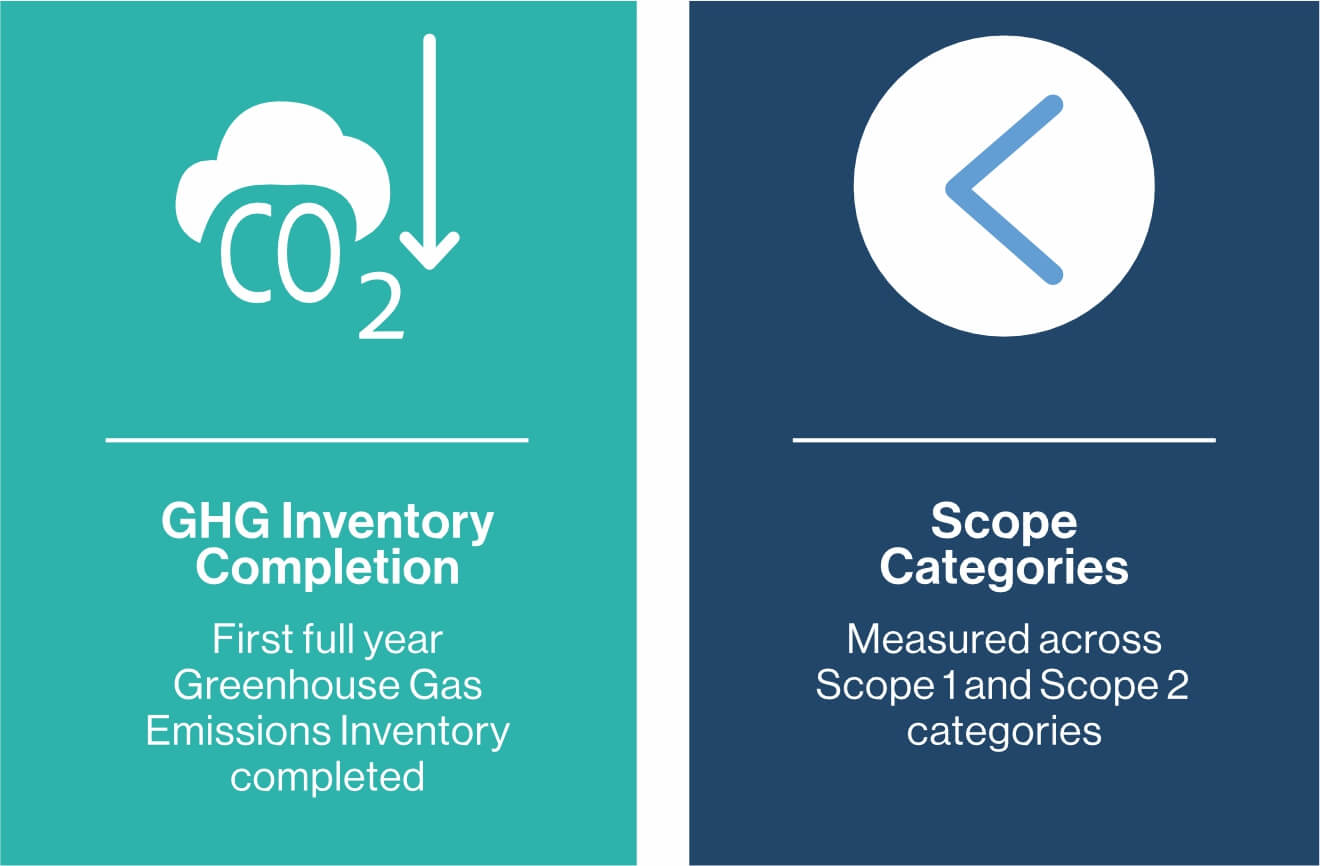

First GHG Inventory (Scope 1 & 2)

We have completed our first full-year greenhouse gas emissions providing a comprehensive baseline to manage and reduce our carbon footprint. For FY24-25, our consolidated emissions were measured across Scope 1 and Scope 2 categories. Scope 1 emissions,which include diesel consumption for backup generators and companyowned vehicles, amounted to 1,742 tCO₂e, while refrigerant-related emissions contributed 168 tCO₂e. Scope 2 emissions from purchased electricity across our offices, branches, and data centers generated 9,484 tCO₂e, constituting 83% of the combined Scope 1 and Scope 2 emissions.

Emission Intensity Analysis

Monitoring emission intensity allows us to understand the environmental impact of our operations relative to our financial performance. For FY2024-25, the energy emission intensity was calculated at 3.77 tCO₂e per crore of turnover. By combining absolute emission data with intensity metrics, we are able to track the effectiveness of energy conservation initiatives and monitor the decoupling of business growth from carbon emissions.

Net Zero by 2040 Commitment

We are committed to achieving net-zero greenhouse gas emissions from our operations by 2040. This target aligns

with the Paris Climate Agreement’s objective of limiting global temperature rise to well below 2 degrees Celsius and striving towards 1.5 degrees Celsius. Our net-zero commitment encompasses absolute Scope 1 and Scope 2 emissions and represents a forward-looking approach to environmental stewardship. Achieving this target will require sustained reductions in operational emissions and a strategic shift toward renewable and low-carbon energy sources across all facilities.

Key Decarbonisation Levers

To achieve our net-zero ambition, we are implementing a multi-pronged decarbonisation strategy focusing on renewable energy, energy efficiency, and technology-driven interventions.

Renewable Energy

Renewable energy is a primary lever in our strategy. We have already begun sourcing renewable energy for key facilities, including our corporate office, and plan to expand this transition across the majority of our offices and branches by 2040. Currently, renewable energy accounts for 593 GJ, representing an initial step toward reducing dependence on fossil-fuel-based electricity.

Energy Efficiency

Energy efficiency is another critical lever. We are systematically replacing .

conventional lighting with LEDs, upgrading HVAC systems, and deploying star-rated energy-efficient appliances in offices and branches. These improvements also support our Scope 2 reduction targets and enhance resource efficiency.

Technology Integration

Technology integration further strengthens our decarbonisation efforts. We employ smart energy management systems, automated lighting and HVAC controls, and real-time monitoring to optimize energy consumption and minimize waste. In parallel, we continue to explore innovative approaches to reduce emissions, including further electrification of company vehicles and adoption of low-carbon office practices

Through our comprehensive GHG inventory, emission intensity analysis, net-zero commitment, and strategic decarbonisation initiatives, we demonstrate an unwavering commitment to environmental stewardship, long-term resilience, and sustainable growth. We will continue to monitor, report, and improve our performance to ensure that our business operations align with global climate objectives and the expectations of our stakeholders.

Water Management

Water Consumption & Footprint

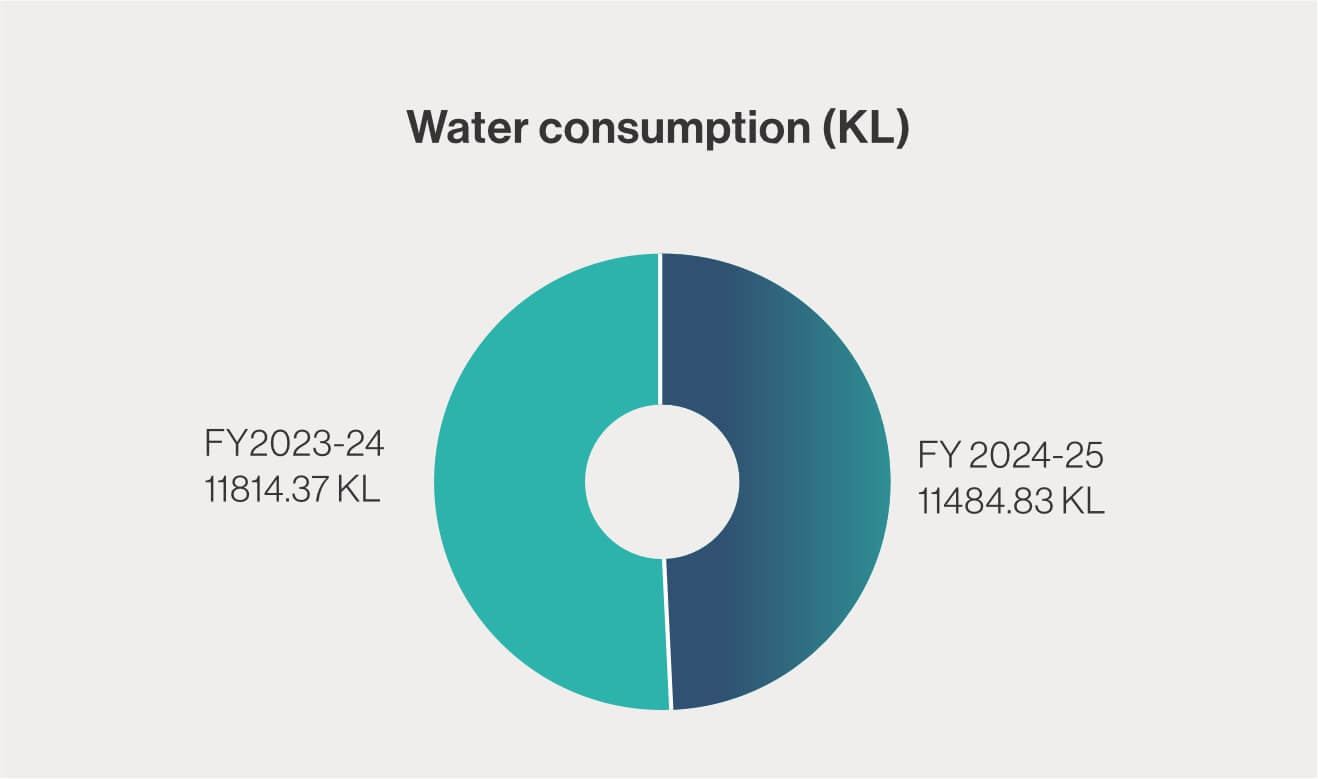

We recognize that water is a finite and shared resource, and effective management of water is a critical aspect of environmental sustainability and responsible business operations. While water is not a direct input for our core banking services, it is essential for employee and customer needs, operational facilities, sanitation, and maintenance. Understanding the importance of water conservation within an ESG-integrated business management system, we have implemented measures to systematically track, manage, and reduce water consumption across all offices, branches, and administrative facilities nationwide.

For the financial year 2024-25, our total water withdrawal and consumption across India amounted to 11,484.83 kilolitres, reflecting a reduction from 11,814.37 kilolitres in FY2023-24. Water consumption has been calculated using a standardized methodology where daily water use per employee is assumed to be 45 litres, consistent with the National Building Code of India, and considering 250 working days annually. This approach provides a comprehensive assessment of our water footprint and enables us to identify opportunities for optimization and efficiency improvements. Water management is guided by globally recognized frameworks such as the Water Resources Institute (WRI) Water Risk Assessment methodology, which allows us to evaluate water-related risks, optimize usage, and ensure sustainable water stewardship across our operations

Efficiency Measures

To improve water efficiency, we have installed low-flow fixtures across our offices and branches, which reduce water demand by approximately 70 percent compared to conventional systems. This is complemented by awareness programs and training for employees, emphasizing responsible water use and conservation practices. By fostering a culture of sustainability within the organization, we ensure that every employee understands the importance of conserving water and actively participates in efficiency efforts.We have also implemented Sewage Treatment Plants (STPs) at our major facilities, including our corporate headquarters. The 90 kilolitres per day capacity STPs treat all wastewater generated on-site, which is then reused for non-potable purposes such as washroom flushing, landscaping, and maintenance activities. This practice achieves zero wastewater discharge from these facilities and significantly reduces freshwater demand. By integrating advanced treatment and recycling systems, we are enhancing operational efficiency while minimizing environmental impact and contributing to sustainable resource management.

Rainwater Harvesting Initiatives

Rainwater harvesting forms a key pillar of our water management strategy. We have installed rainwater collection systems at multiple corporate office buildings to capture and store rainwater for non-potable use. These systems supplement municipal water supply, reduce dependence on groundwater, and manage stormwater runoff, thereby lowering flood risk. By integrating rainwater harvesting with water recycling, low-flow fixtures, and efficient infrastructure, we are systematically reducing our water footprint while promoting sustainable water management practices.

Future Initiatives and Climate Resilience

Looking ahead, we aim to further strengthen our water management strategy by exploring innovative technologies such as smart water meters, automated leak detection systems, and greywater recycling. These initiatives will provide realtime monitoring of water use, identify inefficiencies, and ensure optimized water consumption.

Employee engagement remains central to our water stewardship efforts. Training sessions, workshops, and awareness campaigns will continue to educate our workforce on the importance of water conservation and encourage behavioural changes that complement technological and operational improvements. By fostering a culture of water responsibility, we aim to ensure that all stakeholders contribute to reducing our water footprint and promoting sustainable practices.

Digitisation and Sustainable Resource Consumption

Reducing Paper Consumption: Tangible Environmental Benefits

One of the most significant outcomes of our digital push has been the reduction in paper usage. In FY24, our paperless initiatives led to the saving of 2,97,35,191 sheets of paper, equivalent to nearly 3,498 mature trees. By avoiding paper consumption at this scale, we directly support environmental conservation efforts while also demonstrating our commitment to responsible banking practices.